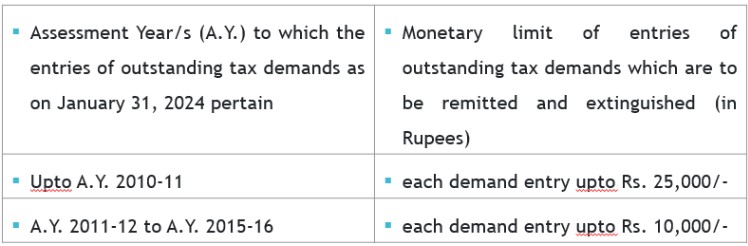

F.No.375/02/2023-IT-Budget: –Remission of Certain Outstanding Direct Tax Demands

The remission of the above outstanding tax demand shall be subject to the maximum ceiling of Rs. 1,00,000/-(excluding calculation of interest on account of delay in payment of demand under the act) for demand entries such as Principal component of tax demand Interest, penalty, fee, cess or surcharge under various provisions of the Act.

Remission and extinguishment of entries of outstanding direct tax demands shall not be applicable on the demands raised against the tax deductors or tax collectors under TDS or TCS provisions of the Income-tax Act. 1961.

Approval of Punjab University for Scientific research under Income-tax Act, 1961, Notification No. 23/2024

The Central Government has approved Punjab University Chandigarh, having PAN AAAJP0325R, for scientific research purposes of 35(1)(ii) of the Income-tax Act, 1961. This approval is effective from the publication date in the Official Gazette (i.e., from the Previous Year 2023-24) and applies for Assessment Years 2024-2025 to 2028-2029.

Climate reporting to help companies ride the green transition.

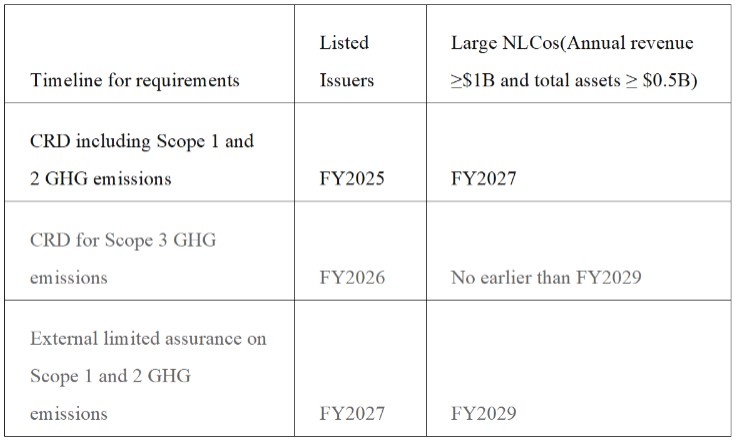

On 28 th February 2024 the Accounting and Corporate Regulatory Authority (ACRA) and Singapore Exchange Regulation (SGX RegCo) have provided details of mandatory climate reporting for listed issuers and large non-listed companies.

As announced by Second Minister for Finance, Mr Chee Hong Tat at the Ministry of Finance Committee of Supply, Singapore will introduce mandatory climate-related disclosures (CRD) in a phased approach, in line with the recommendations from the Sustainability Reporting Advisory Committee (SRAC). This is part of the Government’s efforts to help companies strengthen capabilities in sustainability, and to ride the green transition. As the green momentum intensifies, companies who are able to provide CRD could benefit from access to new markets, customers, and financing.

From FY2025, all listed issuers will be required to report and file annual CRD, using requirements aligned with the International Sustainability Standards Board (ISSB) standards.

From FY2027, large NLCos (defined as those with annual revenue of at least $1 billion and total assets of at least $500 million) will be required to do the same. ACRA will review the experience of listed issuers and large NLCos before introducing reporting requirements for other companies.

The timeline for the implementation of mandatory CRD is summarised in the table below, with an accompanying infographic in the Annex. More time will be given for companies to report CRD on Scope 3 greenhouse gas (GHG) emissions and conduct external limited assurance on Scope 1 and 2 GHG emissions.

Some companies have provided feedback that they are already reporting using other international standards and frameworks, to meet mandatory requirements of the

jurisdictions that they operate in and/or to cater to their investors’ information needs. To address this, ACRA will exempt large NLCos with parent companies that are reporting CRD, under the following circumstances:

a) A large NLCo whose parent company reports CRD using ISSB-aligned local reporting standards or equivalent standards (g. European Sustainability Reporting Standards) will be exempted from reporting and filing CRD with ACRA, subject to certain conditions; and

b) A large NLCo whose parent company reports CRD using other international standards and frameworks (g. Global Reporting Initiative Standards, Task Force on Climate-related Financial Disclosures Recommendations), will be exempted from reporting and filing CRD with ACRA2 for a transitional period of 3 years, from FY2027 to FY2029. ACRA will review whether to extend the transitional period, depending on global developments relating to the adoption and recognition of other standards and frameworks.