CBDT notifies annual circular for TDS on salaries for FY 2020-21

Circular No. 20/2020 dated 03 December 2020

• As has been the practice every year, the CBDT notifies annual circular for TDS on salaries for FY 2020-21

• Under the circular, CBDT clarifies procedure and gives examples for the computation of tax deducted at sources on salary under section 192.

CBDT issues second set of FAQs on Vivad se Vishwas Scheme

Circular No. 21/2020 dated 04 December 2020

• CBDT’s second set of 34 FAQs on Vivad se Vishwas Scheme further clears air on:

• The scope/eligibility (20 FAQs), • Computation (4 FAQs), • Consequences (8 FAQs) and • procedure (2 FAQs);

• Clarifies on availability of the Scheme where appeal / arbitration was pending as on the specified date (i.e., Jan 31st, 2020), but was subsequently disposed off before filing of declaration;

• Further, clarifies that where the application for condonation is filed before the date of issue of this circular, and appeal is admitted before the date of filing of the declaration, “such appeal will be deemed to be pending as on 31st Jan 2020.”;

• Also, issues clarification on Scheme entitlement in respect of cases before AAR and cases where MAP is invoked, states that “in a case where MAP resolution is pending or the assessee has not accepted MAP decision, the related appeal shall be eligible for VsVS.”;

• However, makes it clear that appeal against Trust’s registration denial is not eligible for VsVS;

IT Department releases FAQs on quoting UDIN in audit reports and CA certificates

Dated 09 December 2020

• Reiterates that UDIN is mandatory for uploading audit report and CA certificates on the e-filing portal. • Clarifies that uploading various documents is possible without generating UDIN, however, UDIN generated for the form should be updated to avoid the form uploaded being treated as invalid within 15 calendar days of uploading. • Appraises procedure for correction of errors in a form where UDIN has already been updated. Clarifies on the impact of revoking UDIN after the form is accepted by the taxpayer. • As on 14/12/2020- a One-time relaxation to update UDIN has been enabled to update the UDIN of audit report/certificates before 31st December, 2020 to avoid invalidation. • As a One-time condonation scheme, to regularize the non-generation of UDIN, the ICAI has now allowed CAs to generate UDINs missed for the documents signed between 1st February, 2019 to 31st December, 2020. The scheme will be made available from 1st January, 2021 till 31st January, 2021.

Yamuna Expressway Authority notified under sec. 10(46)

Notification No. 91/2020/F.No.300196/4/2014-ITA-I, 24th December 2020

• Pursuant to Delhi HC Order in matter of Yamuna Expressway Industrial Development Authority (YEIDA) dated 23rd August 2020.

• In exercise of the power conferred by section 10(46) of the Income-tax Act, 1961, YEIDA (PAN AAALT0341D) is notified as an authority constituted by the UP State Government, in respect of the specified income arising to that Authority, namely grants, money from the disposal of properties, rentals, interest earned and penalties received various movable or immovable properties.

IT Department releases instructions for XML generation using Java utility for tax filing

Dated 14 December 2020

• In order to cater to the needs of its users/taxpayers, the Income-tax Department releases instructions to download and use the Java utility for generation of XMLs and calculation of tax more accurately.

• With the continuous up gradation brought out in the version of Microsoft Office, Income-tax Department also felt the need to solve the problems faced by users to generate XMLs for filing their return of income in the absence of Microsoft Office 2010 or its later version.

• The IT Department has released a 13-step instruction guide to download the Java utility, then generate the XML and upload the same on the income tax portal.

Case Laws

Kar HC: Expense reimbursement on seconded employees - Not Fees for Technical Services (FTS), No TDS; Distinguishes Centrica

Director of Income-tax Vs ABBEY BUSINESS SERVICES INDIA PVT. LTD., ITA No.214 of 2014, 01st December 2020

• Karnataka HC upholds ITAT order; holds that payment made by assessee-company (Abbey India) during AY 2005-06 to its UK Group Company (ANP) towards reimbursement of hotel and travelling expenses incurred on seconded employees is not FTS and thus, not liable for TDS u/s 195;

• ANP entered into a secondment agreement with assessee to facilitate the outsourcing agreement between ANP and a third-party service provider in India and deducted TDS on salary reimbursed exclusive of the hotel and travelling expenditure; Stating that the employees of ANP seconded to India were highly skilled technical personnel, Revenue held that the entire payment made was in the nature of FTS u/s 9(1)(vii) and also under Art. 13 of India-UK DTAA;

• Observes that under the agreement, the seconded employees have to work at such place as the assessee may instruct and function under the control, direction and supervision of the assessee in accordance with the policies, rules and guidelines applicable to the employees of the assessee;

• Remarks that “the assessee for all practical purposes has to be treated as the employer of the seconded employees.”; Opines that there is no obligation in law for deduction of tax at source on payments made for reimbursement of costs incurred by a non-resident enterprise and therefore the amount paid by the assessee was not amenable to withholding u/s 195;

• Holds that the expenses reimbursed to the seconded employees by the assessee is not liable to TDS as not covered under FTS; Distinguishes Delhi HC ruling in Centrica India and states that “the issue of permanent establishment is not involved. Therefore, the aforesaid decision is not applicable to the fact situation of the case.”

ITAT: Advertisement payments to Facebook not claimed as business expenditure can't be disallowed for non-withholding

Interactive Avenues Private Limited vs Deputy Commissioner of Income Tax, Circle 14(2)(1), Mumbai, ITA No.: 3130/Mum/19, dated 01 December 2020

• Mumbai ITAT ‘in principle’ upholds assessee’s (an advertisement agency in India) plea that its payments to Facebook Ireland Ltd. during AY 2015-16 towards the cost of advertisements, for its clients cannot be subjected to disallowance u/s. 40(a)(i) for TDS default “when the related expenditure is not claimed as deduction…”;

• ITAT remits the matter for the limited purpose of factual verification of whether “the assessee has indeed accounted for the agency commission on these advertisement revenues, rather than taking entire billing revenues as billing revenues of the assessee and claiming a deduction for the advertisement paid to Facebook Ireland Limited in its profit and loss account.”;

• ITAT takes note of assessee’s claim that it receives and accounts for agency commission of 15% on net billings as revenue with no simultaneous claim of deduction on amount paid to Facebook.

ITAT: Restricts TP-adjustment on AE-loan to higher of LIBOR and assessee’s rate of interest

• ITAT adjudicates on TP-adjustment in respect of interest on loan advanced to the AE by assessee for AY 2012-13

• In respect of interest on loan, ITAT notes that assessee advanced money to its sister concern after availing loan from SBI which charged interest at 8.28% and charged the same interest to its AE

• Observes that, however, TPO charged interest at 14.47% and made TP adjustment at Rs.1.50 crores;

• Noting assessee’s submission that the interest rate of 8.28% p.a. is more than LIBOR, ITAT remits the issue back to AO/TPO by stating that “AO has to examine LIBOR rate in the specific transaction under consideration and if it is more than 8.28%, the same is to be charged otherwise the rate at which assessee advanced should be applied”

Mumbai ITAT construes share application money as capital asset; Allows setting off capital loss

DCIT Vs Morarjee Realties Ltd, ITA No.2343/Mum/2009, 15-Dec-2020

• Holds share application money transferred along with the equity and preference shares within the group in corporate restructuring as a capital asset;

• Assessee incurred short term and long-term capital loss on the transfer of shares and the right to apply for shares (share application money);

• CIT(A) granted relief to the assessee but limited the set-off of capital loss only to shares and held that share application money was not capital asset u/s 2(14);

• ITAT follows HC ruling and remarks that ‘capital asset’ means property of any kind with the specific exclusion of stock-in-trade, consumables or raw materials held for business purposes. Held ‘property’ has the widest import;

• Holds that share application as transferred/assigned would constitute “advances till the time the shares are allotted and share application money is converted into share capital” and hence capital asset u/s 2(14).

HC: Benefit arising on surrender of Keyman Insurance Policy (KIP) taxable as perquisites in hands of the employee

Allu Arvind Babu v. ACIT dated 04 December 2020

• Assessee was Managing Director of a Company which had taken 2 keyman insurance policies (KIP) on his life. Out of these policies, one policy was assigned in favour of assessee on which he offered surrender value of such policy to tax as perquisite in the year of the assignment itself.

• Subsequently, he encashed the policy at a price higher than the surrendered value. AO made additions for the differential amount to the income of assessee.

• Assessee contended that sum received on encashment of policy was not taxable as it was an ordinary life insurance claim received by assessee which was exempted under Section 10(10D).

• On appeal, the Delhi HC held that the character of Insurance policy does not change after its assignment. Assessee himself had never paid any premium on the said KIP from his resources. Therefore, even if the assignment is endorsed by the Insurance Company, the character of the Policy does not convert into an ordinary Life Insurance Policy in the hands of Assessee.

• Further, based on Section 10(10D) with its Explanation 1, the clear position of law which emerges is that the character of the KIP does not get converted into ordinary Life Insurance Policy despite its assignment and therefore, any benefit accruing to the employee upon its surrender or encashment will be taxable in the hands of the Employee as perquisite.

ITAT: Interest on the sum borrowed to repay a loan utilised for construction of commercial property deductible u/s 24(b)

Indraprastha Shelters Pvt. Ltd. Vs DCIT, ITA No.2597/Bang/2019, 18th December 2020

• Bangalore ITAT allows the deduction of interest u/s 24(b) on loan taken to repay another loan utilised for the construction of a commercial building; Follows CBDT Circular No. 28 dated 20-08-1969 to hold that proviso to Sec. 24(b) only refer to ‘property’.

• Assessee, a developer and builder, declared income from house property after claiming a deduction on interest paid on capital borrowed from Mrs. Kaveri Bai utilised to repay the loan taken from Corporation Bank in the construction business

• ITAT observes that Revenue disallowed interest relying on the third proviso to section 24(b) which provides that furnishing of a certificate from the lender specifying details of interest and capital borrowed is required to grant deduction; ITAT acknowledges Assessee’s contention that the Circular permitting deduction of interest paid on loan taken to repay another loan for computing income from house property issued for erstwhile Sec. 24(1)(vi) holds good under the current provisions

• Sets aside CIT(A) order upholding disallowance made by Revenue on the premise that the Circular was not applicable as it was issued for provisions applicable before 1.4.2002; Extends applicability of the Circular to the current day provisions,

• ITAT highlights that the deduction of interest is allowable irrespective of whether the property under question is residential or commercial; Holds that “The proviso only carves out an exception to section 24(b) of the Act, in so far as it relates to property used for residential purposes and does not deal with or curtail the right of an assessee to get a deduction on interest paid on loans borrowed for the purpose of constructing commercial property”

Delhi ITAT deletes addition of ₹219 Crores as Gift of shares held as stock-in-trade not taxable as business income

Manjula Finance Ltd Vs ITO, ITA No.3727/Del/2018, 18-Dec-2020

• Delhi ITAT holds that gift of shares, held as stock-in-trade, by assessee (O.P. Jindal Group Co.) to its sister concern cannot be charged to tax as business income in the absence of any consideration.

• Revenue had held that the gift of shares for AY 2014-15 was a tax evasion scheme since the shares were held as stock in trade, taxed ₹219 Cr (excess of FMV over the cost of such shares) as business income.

• ITAT Observes that only real income can be taxed in the hands of the assessee and there is no scope for taxing any hypothetical income unless law mandates to do so;

• ITAT remarks that ‘As the assessee has gifted the share, there is no accrual of any revenue to the assessee’ viz. there is no cash inflow, receivables or other consideration to the assessee.

Non-Disclosure of Foreign Bank Accounts

19th December 2020

• Additional Chief Metropolitan Magistrate (Special Acts), Delhi (ACMM), discharges Pradip Burman of Dabur Group and Ashok Jaipuria (accused-assessees) of offences u/s 277 / 276C of Income-tax Act for allegation of stashing money in the foreign bank accounts made by relying on the base notes received from abroad could not pass the test of prosecutable evidence.

• Prima facie case of tax evasion was made out by Revenue against Mr. Burman and Mr. Jaipuria, using the information received by CBDT from the French and Liechtensteiner authorities, for being beneficiaries of bank accounts in HSBC Bank, Switzerland and LGT Bank, Liechtenstein, respectively.

• Reassessment notices for taxing the undisclosed foreign income and prosecution notices for offence punishable u/s 277 / 276C were issued simultaneously to the accused-assessees that resulted into complaints in which discharge applications were preferred by the accused-assessees.

• ACMM observes that ‘Perusal of the aforesaid documents…reveals that even a slight inference cannot be drawn to the effect that it was the accused who opened the said bank account or that he was having any knowledge that the said bank account is in existence.’ • On Revenue’s stand on the presumption of culpable mental state as per Sec. 278E, ACMM clarifies that ‘without first discharging the burden of establishing the foundational facts, the prosecution cannot take benefit of the statutory presumption of the culpable mental state against an accused.’

ITAT: Revenue's appeal for TDS u/s 195 on CCD interest against Coffee Day lacks aroma

DCIT Vs Coffee Day Enterprises Ltd., ITA No.2931/Bang/2018 & C.O. No. 42/Bang/2019, 22nd December 2020

• Bangalore ITAT dismisses Revenue’s appeal for AY 2011-12, holds that withholding u/s 195 is not required where annual interest on compulsorily convertible debentures (CCD) was neither paid to the Cypriot investor by Coffee Day Enterprises Ltd. (assessee) and nor was it claimed as an expenditure;

• Rejects Revenue’s contention that interest was accrued on grounds that the Cypriot investor waived the interest; Holds that the term ‘paid’ in the India-Cyprus DTAA “is to be interpreted as intended to be taxed on a paid basis and not on an accrual basis”

• Holds that “the purpose of deduction of tax at source is not to collect a sum which is not a tax levied under the Act, it is to facilitate the collection of tax lawfully leviable under the Act”; Regarding limitation u/s 201, holds that order made after the expiry of seven years from the end of the relevant financial year was not made within a reasonable time.

• Revenue passed Sec. 201 order against assessee for failure to deduct tax at source; CIT(A) upheld Assessee’s appeal that TDS liability did not lie since no interest was paid in the relevant AY, no interest was claimed as expenditure but was deferred and eventually waived by the investor under an agreement.

Delhi HC: Sets aside ex-parte order favoring Revenue

Kalra Papers Private Limited Vs ITO, W.P.(C) 9467/2020, 24-12-2020

• Delhi HC sets aside ITAT’s ex-parte order passed in Revenue’s favour and restores the appeal

• HC was satisfied that the assessee was prevented by sufficient cause from appearing before the ITAT when the appeal was taken up for hearing;

• Further holds that “We are also persuaded to allow the petition, in view of the undertaking given by the Petitioner that it would apply under the ‘Vivad Se Vishwas’ Scheme in the event the appeal is restored to its original number.”;

• ITAT dismissed questioning interest of the appellant since it sought adjournments;

• HC remarks that “The presumption of disinterest against the Petitioner is speculative”; and holds that where sufficient cause for nonappearance is shown later, ITAT is obligated to consider the same.

Delhi HC provides relief to Manpower Group Services India Pvt. Ltd.

Manpower Group Services India Pvt. Ltd. VS CIT (TDS)

W.P. (C) 5865/2020 & CM APPL. 21184/2020, 24th December 2020

• Delhi HC quashes AO’s order u/s 197 refusing to grant a ‘Nil’ rate TDS certificate to assessee -petitioner (engaged in providing manpower related services), cites non-application of mind by AO;

• At the outset, HC rejects Revenue’s stand that the writ petition was not maintainable: Holds that since the impugned order was passed after approval from CIT on the TRACES portal, it cannot be challenged by way of a revision petition before CIT u/s 264;

• Also, holds that the decision-making process in the present case is contrary to law, cites Rule 28AA (which outlines the procedure for determining the TDS rate for Sec. 197 purposes) and, observes that the AO did not bring on record the computation of TDS rates under Rule 28AA; Remands matter to AO.

• In the interim directs providing the benefit of revised TDS rates along with 25% rebate on account of Covid crisis.

Kol ITAT: Transfer of tenancy rights to be taxed as capital gains

DCIT Vs Smt. Shikha Roy, ITA No.1915/Kol/2019, 25-11-2020

• Assessing Officer (AO) disallowed the assessee’s claim of deduction u/s 54EC and 54F on the view that the amount received was in the nature of compensation for vacating tenancy taxable as Business Income.

• The AO contended a) lack of proof of rent payments; b) loan provided to landlord for construction cannot be considered as the cost of acquisition; c) Even if held as Capital asset transfer, cost of acquisition would be ₹ 0.

• ITAT based its judgement referring the case of A. Gasper vs. CIT (Kol), affirmed by the SC, that the monthly tenancy of the assessee was a capital asset as defined u/s 2(14) of the Income Tax Act.

• Thus, the ITAT favoured the assessee, treating the transfer of tenancy rights as the transfer of capital assets and held loan given was the cost of acquisition of such rights.

International Arbitration

Cairn Energy wins $1.6 Bn tax arbitration against India

23rd December 2020

• As per Reuters, Cairn Energy has won an international arbitration case against the Indian government over a tax dispute involving $1.6 billion;

• Cairn Energy Plc and its subsidiary Cairn UK Holdings Ltd. (Claimants) win international arbitration on tax dispute with India under India-UK BIPA;

• Arbitral Tribunal rules that India failed to uphold its obligation under the UK-India BIT and international law, and in particular, that it has failed to accord the Claimants’ investments fair and equitable treatment in violation of Article 3(2) of the Treaty;

• Arbitral Tribunal orders India to compensate the claimants for Rs. 8,842 crores due to the breach of treaty obligations.

• Decision was rendered by the permanent court of Arbitration, holding that issue was under its jurisdiction.

India challenges Vodafone arbitral award in Singapore Court

24th December 2020

• India has challenged the arbitral award before Singapore Court which ruled that tax demand from Vodafone based on a retrospective legislation was in the “breach of the guarantee of fair and equitable treatment” guaranteed under India-Netherlands Bilateral Investment Treaties (BIT)

Other updates/News

IT department detects black income of ₹ 100 crores after raids on contractors

26th December 2020

The income tax department started searches at 14 multiple locations of a group of 3 leading contractors of north eastern India.

Allegations:

• The group have taken accommodation entries in the form of non-genuine unsecured loans from Kolkata based shell companies, that exist only on paper and have no real business and creditworthiness.

• Also learned that one of the groups carries out as high as 50% of its hospitality business in cash and that some of the entities of the groups also engage in purchases of Jewellery in cash.

Findings:

• Unaccounted income of about ₹65 crores of the group was routed • Jewellery worth ₹9.79 lakh has been seized with sources of over ₹2 crores still under verification • Cash of Rs 2.95 crore has also been seized • Overall, undisclosed income to the tune of approximately Rs. 100 crore has been unearthed so far during the Search and Survey operation. Further investigations are under progress

Other Updates

• CBDT introduced “jhatpat processing” for ITR-1 and ITR-4 in cases where there is no arrears, no income discrepancy, no TDS or Challan mismatch, ITR is verified and bank account is validated. Lead time mentioned is 2 days.

News of the hour

• ITAT announces transfer of 7 members with immediate effect on December 11, 2020

• Shri Chandra Poojari – From Cochin to Bangalore

• Shri Kul Bharat – From Indore to Delhi

• Shri Sanjay Garg – From Chandigarh to Kolkata

• Shri Satbeer Singh Godara – From Kolkata to Hyderabad

• Shri Laxmi Prasad Sahu – From Cuttack to Hyderabad

• Shri Ram Lal Negi – From Mumbai to Chandigarh

• Shri Narendra Kumar Choudhry – From Amritsar to Visakhapatnam

• CBDT issues refunds of over Rs 1,45,619 crore to more than 89.29 lakh taxpayers between 1st April 2020, to 08th December 2020.

• Supreme Court to decide the constitutional validity of ICAI’s cap on the number of tax audits a practising CA can conduct.

• OECD’s Global Forum on Transparency and Exchange of Information for Tax Purposes releases peer review report, reveals that satisfactory legal framework to implement automatic exchange of information (AEOI) have been put in place with a continuing effort to monitor processes to assess its effectiveness in 100 jurisdictions.

Goods and Services Tax

With an objective to curb tax evasion and menace of fake invoices, the Government has introduced various measures in GST law right from the process of registration, GST payment in cash in select cases, claiming input tax credits etc. The same are summarized below.

Biometric-based authentication to obtain GST registration

Government has introduced biometric-based Aadhar authentication or verification of biometric information (in case of the non-Aadhar route) to obtain GST registration. Earlier Aadhar authentication through OTP route was sufficient for quick processing of GST registration in 3 days.

Under the new rules, in addition to verification of biometric information, taking a photograph of the authorized signatory and verification of original documents at one of the notified facilitation centres is also required. With this, the processing time of registration is increased from 3 days to 7 days now.

Further, physical verification of business premises will be mandatory in case the applicant has not opted for Aadhar authentication.

This change will be effective from a date to be notified in future.

Suspension and Cancellation of GST registration

From 1 January 2021, GST registration may be suspended without prior notice if:

• Turnover in GSTR-1 is greater than that declared in GSTR-3B;

• Input tax credit in GSTR-3B is greater than that appearing in GSTR-2A report;

• Failure to make GST payment in cash as specified in new Rule 86B

It is pertinent to note that, during suspension, taxpayer cannot issue tax invoice and collect GST as well as cannot generate e-way bill. In case taxpayer is not able to justify the above lapses on his part then his registration may be cancelled by the GST officer.

Government revises provisional input tax credit limit from 10% to 5%

Rule 36(4) of the Central GST Rules have been amended from 1 January 2021 to restrict the provisional input tax credit claim to 5% of the matched credits. It appears that the Government is moving towards allowing only matched credits to the taxpayers.

Non-filing of GSTR-3B would result in blocking of GSTR-1 or IFF

From 1 January 2021, taxpayer would not be able to file his GSTR-1 or access Invoice Furnishing Facility if he has not filed GSTR-3B for preceding two months. Earlier, non-filing of GSTR-3B used to result in blocking of e-way facility. It appears that the intention here is to prevent businesses from passing on input tax credit if they have not paid GST liability.

Mandatory 1% GST payment in cash for select businesses

From 1 January 2021, a business having their taxable turnover more than ₹ 50 lakhs in a month have to mandatorily pay at least 1% of their GST liability in cash. In other words, they can use their input tax credits only up to 99% of their GST liability.

However, the Government has duly provided an exemption to following bonafide cases from the applicability of this new rule. • The taxpayer or his Managing Director or Whole-time Director or any of its two Partners have paid more than one lakh rupees as income tax in each of the last two financial years; or •The taxpayer has received a refund of an unutilized input tax credit of more than one lakh rupees in the preceding financial year on account of exports; or • The taxpayer has received a refund of an unutilized input tax credit of more than one lakh rupees in the preceding financial year on account of inverted duty structure; or • In the current financial year, the taxpayer has paid at least 1% of his total output tax liability (applied cumulatively) through electronic cash ledger; or • The taxpayer is a government department or PSU or local authority or statutory body.

It is also worthwhile to note that in other genuine cases not covered above, the Commissioner of GST may remove this restriction after such restrictions and safeguards as he may deem fit.

With these new amendments, while the intent of the Government to make tax evasion impossible, is laudable, the implementation of the same in its true letter and spirit will be a key for its successful implementation.

E-way bill validity reduced

From 1 January 2021, the validity of e-way bills has been narrowed. Earlier e-way bill was valid for a day for a distance up to 100 kms. This distance is now increased to 200 kms. To illustrate, for a distance up to 600 kms, earlier e-way bill validity was 6 days, now only 3 days will be allowed for the same distance.

Thus, the businesses have to be watchful now to ensure that goods movement is completed within the new narrowed timelines else e-way bill validity needs to be extended before its expiry.

GSTN issues advisory on auto-population of e-invoice details into GSTR-1

The data from e-invoice portal is now auto-populated in GSTR-1 return on T+3 days basis. For example, e-invoice for which IRN is generated on 26th December 2020 would be auto-populated in GSTR-1 on 29th December 2020. However, owing to certain validations in GSTR-1, e-invoices with below observations would not be auto-populated in GSTR-1:

i. Invoice date is prior to Supplier’s/Recipient’s effective date of registration;

ii. The invoice date is after Supplier’s/Recipient’s effective date of cancellation of registration;

iii. Invoices reported as attracting “IGST on Intra-state supply” but without reverse charge

Communication between Recipient and Supplier Taxpayers on GST Portal

A facility of ‘Communication Between Taxpayers’ has been provided on the GST Portal, for sending a notification by recipient (or supplier) taxpayers to their supplier (or recipient) taxpayers, regarding missing invoices/debit/credit notes or any shortcomings in these documents or any other issue related to it.

Customs Update

Government extends Remission of Duties and Taxes on Exported Products (RoDTEP) benefit to all export goods from 1 January 2021

Taking a major step to boost exports from India, Government has decided to extend RoDTEP benefit to export of all goods with effect from 1 January 2021. The RoDTEP scheme would refund to exporters the embedded Central, State and local duties/taxes that were so far not being rebated/refunded and were, therefore, placing exports from India at a disadvantage. The refund would be credited in an exporter’s ledger account with Customs and can be used to pay Basic Customs duty on imported goods. The credits can also be transferred to other importers.

The RoDTEP rates would be notified shortly by the Department of Commerce. An exporter desirous of availing the benefit of the RoDTEP scheme is required to declare his intention for each export item in the shipping bill or bill of export. The RoDTEP would be allowed, subject to specified conditions and exclusions.

Customs duty drawback claims to be processed within 3 days

CBIC instructs faster processing of duty drawback claim within 3 days (T+2 basis) to the bank account of the exporters. Earlier in March 2020, CBIC had instructed customs officials to dispose of all remaining customs duty drawback claims by end of March 2021 and target was set to process claim within 7 days. Now, further accelerating this target to 3 days would indeed benefit exporters.

Customs Faceless Assessments – clarification issued by Government

Principles of natural justice to be followed in case of reassessment

Central Board of Indirect Taxes and Customs (CBIC) has clarified that while re-assessing the bill of entry (happens when self-assessment done by the importer is rejected by the customs officer) it must be ensured that importer is given an opportunity to justify the self-assessment either in writing or through video conferencing. Further, customs officer is required to issue speaking order (to enable the importer to seek appeal remedy) in case he rejects self-assessment of the importer.

Importers advised to mention complete description of the imported goods

One of the main reasons which delays the verification process and clearance of imported goods is that importers do not give a complete description of the imported goods while filing bill of entry. Towards this CBIC has advised importers to use following fields that are available in the electronic Bill of Entry format:

i. Generic description of imported goods: Description which is line with exemption notification / IGST levy / Anti-dumping duty may be provided in this field

ii. Specific description: The description specific to the product and mentioned in the import Invoice along with trade name can be provided here

iii. Model and brand name: Model details and brand name may be provided in this field and in case imported goods are unbranded then the text “unbranded” may be used.

iv. Previous bill of entry: If the subject goods are already imported earlier, then the details of the previous bill of entry may be given for reference.

Supporting documents to claim duty exemption to be compulsorily uploaded in e-Sanchit

CBIC has also decided that for faster processing of import shipments, with effect from 15 January 2021 importers would be required to upload in e-Sanchit the supporting documents to justify their claim of duty exemption.

CBIC enhances monetary limit for assessment of bill of entry

To expedite the assessment process, CBIC has decided to enhance the monetary limit for assessment by Appraising Officer from the present limit of ₹ 1 lakh to ₹ 5 lakhs from 21st December, 2020. Bill of Entry with an assessable value above ₹ 5 lakhs would be subject to two-step scrutiny, first by the Appraising Officer and then by the Deputy/Assistant Commissioner of Customs.

Due Dates

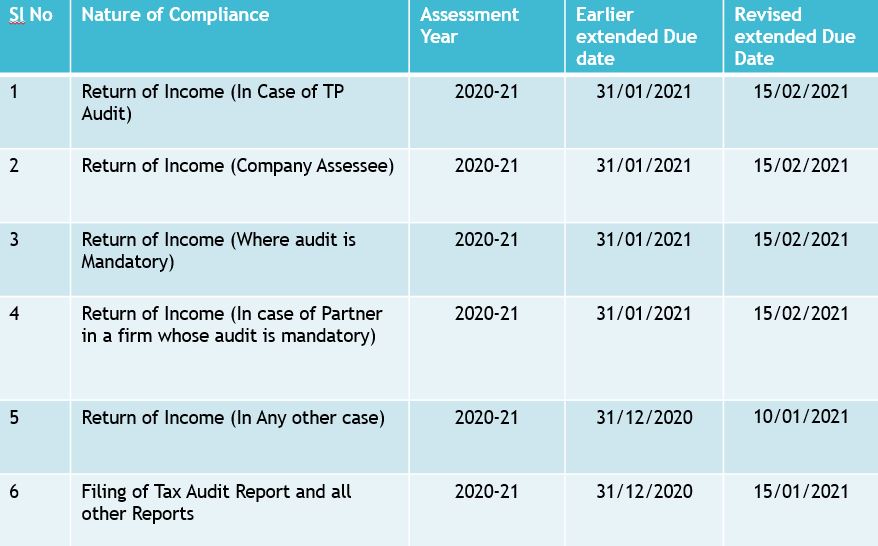

Extension of Due Date of furnishing of Income Tax Return and Audit Reports

Press Release, 30th December 2020

• Considering the hardships and challenges faced by taxpayers, the CBDT has further extended the due dates of filing of Income tax return and due date of furnishing of Audit report as follows.

• Relaxation from interest under section 234A of the Act

• In order to provide relief to small and middle-class taxpayers in the matter of payment of self-assessment tax, the deadline for payment of self-assessment tax date has also been further extended.

• Accordingly, if the self-assessment tax (i.e., after reducing tax deducted/collected at source, advance tax etc.) does not exceed Rs.100,000/-, then there shall be no interest if such tax is paid by the extended due date of filing tax return i.e., 10 January 2021 or 15 February 2021 , as the case may be.

• Relaxations under Vivad Se Vishwas Scheme

• The last date for making a declaration under Vivad Se Vishwas Scheme has been extended to 31st January 2021 from 31st December 2020.

• The date of passing of orders under Vivad se Vishwas Scheme, which are required to be passed by 30th January 2021 has been extended to 31st January 2021.

• Relaxation for passing orders or issuance of notice under the direct taxes or benami acts:

• The deadline for passing order or issue notice has been further extended to 31 March 2021.

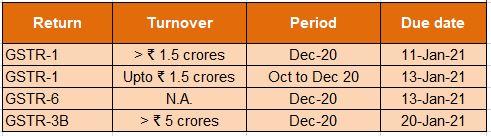

GST Compliance calendar

Category 1 States: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

Category 2 States: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi

SINGAPORE UPDATES

Accounting and Corporate Regulatory Authority (ACRA) Latest Updates

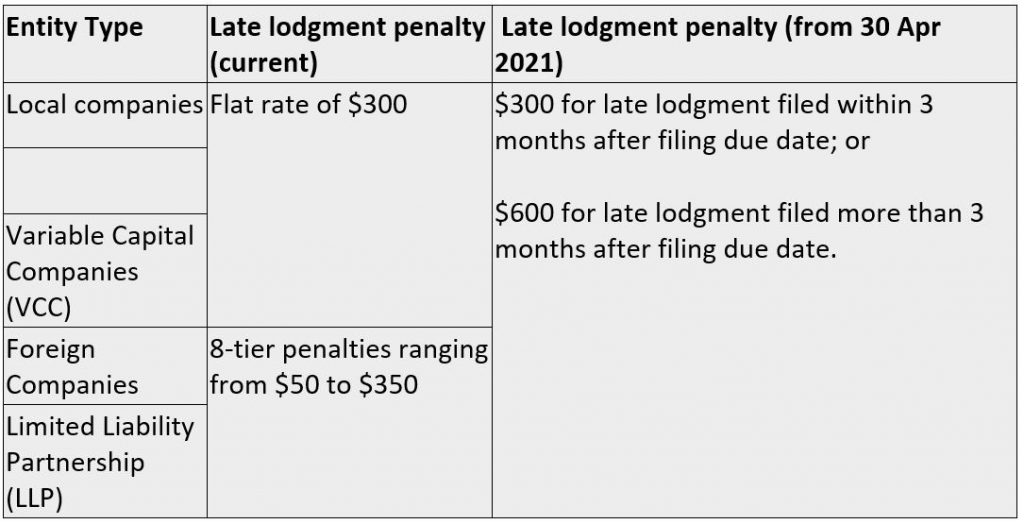

1) Revised Penalty Framework for Annual Lodgments to take effect from 30 Apr 2021

Under the legislations administered by ACRA, all Singapore incorporated companies, Variable Capital Companies (VCCs) and Limited Liability Partnerships (LLPs) are required to file annual lodgment including annual returns and annual declarations with ACRA, within a prescribed timeline. A late lodgment penalty will be imposed against companies, VCCs and LLPs for the late filing of annual returns and annual declarations.

ACRA has revised the penalty framework for late annual lodgments with a simplified 2-tier penalty, to take effect from 30 Apr 2021. This is part of ongoing efforts to make compliance simple and to encourage companies and LLPs to take their statutory obligations on annual reporting seriously.

There is no change to the current penalty framework for ad hoc filings.

Under the revised penalty framework, all Singapore-incorporated companies, VCCs and LLPs will be imposed with a late lodgment penalty of $300 if the annual return or annual declaration is filed within 3 months after the filing due date, or $600 if the lodgment is filed more than 3 months after the filing due date.

Please refer to the revised penalty framework as set out in the table below.

The timely filing of annual lodgment is an important statutory requirement as this ensure timely public disclosure of key information such as the health and status of the entity. All companies and LLPs are advised to file annual lodgment on time to avoid incurring late lodgment penalty.

2) Extension of the effective date for revised XBRL filing requirements to 1 May 2021

On 16 May 2020, ACRA announced the revised filing requirements for companies required to file financial statements in eXtensible Business Reporting Language (XBRL) format, which would take effect from 1 Jan 2021. Companies can opt to voluntarily adopt the revised XBRL filing requirements when filing financial statements from 16 May 2020 to 31 Dec 2020.

In view of the challenging economic situations amid the COVID-19 pandemic, ACRA is providing a one-off extension to give companies more time to adopt the revised filing requirements and data elements for the filing of financial statements in XBRL format as follows:

• Companies are required to apply the revised XBRL filing requirements and data elements from 1 May 2021; and

• Companies can opt to voluntarily adopt revised XBRL filing requirements and data elements up till 30 Apr 2021.

ACRA urges all companies to voluntarily adopt revised XBRL filing requirements early as most companies would be able to benefit from a reduced number of data elements that they need to file with ACRA under the revised XBRL requirements.

In line with the Smart Nation initiative to help SMEs stay relevant and competitive, ACRA and the Inland Revenue Authority of Singapore (IRAS) have partnered accounting software providers to co-create a new digital solution that allows SMEs to automate the preparation and filing of statutory filings with ACRA and IRAS seamlessly.

The seamless filing solution incorporates the requirements for filing tax and annual returns into the accounting software, allowing companies to record their operating transactions and generate the required statutory filings using the accounting software. The software is linked to ACRA and IRAS via Application Programming Interfaces (APIs), which enables companies to file their statutory filings without the need to log in to ACRA and IRAS portals.

Form C-S/C for the FY 2020 -30-November-2021 Estimated Chargeable Income (ECI) (Dec year-end)- 31-Mar-2021 GST Return October- December 2020 – 31-January-2021