ECB 2 Returns for the month of January 2021 to be filed on or before 7 February 2021.

Corporate Social Responsibility (CSR) updates:

1. Vide a notification dated 22 January 2021, MCA has notified amendments made by the Companies

Amendment Act, 2019 to Section 135 of the Companies Act 2013:

• Unspent CSR amount, if any, has to be transferred to a Fund specified in Schedule VII, within a period of six months of the expiry of the financial year. • Unspent CSR amount for ongoing projects has to be transferred to a special bank account within 30 days from the end of the financial year and such amount shall be spent by the company within three financial years from the date of such transfer, failing which, the company shall transfer the same to a Fund specified in Schedule VII, within 30 days from the date of completion of the third financial year.

2. Vide another notification dated 22 January 2021, MCA has

notified amendments made by the Companies Amendment Act,

2020 to Section 135 of the Companies Act 2013:

• Excess CSR expenditure may be carried forward and set off subject to compliance with certain conditions.

• In case the CSR amount to be spent does not exceed ₹ 50 L, the requirement for the constitution of the Corporate Social Responsibility Committee shall not be applicable.

• Penal provisions are introduced for non-compliance of CSR provisions with respect to minimum CSR spend and transfer of unspent amount.

3. MCA has issued Companies (Corporate Social Responsibility Policy) Rules, 2021 vide notification dated 22 January 2021.

• In house activity of R&D in relation to Covid-19 medicine may be included in the CSR Activities subject to compliance with certain conditions.

• Entities which may undertake CSR Activities is introduced with additional conditions. Further mandatory registration with MCA is included. Any new CSR project after 1 April 2021 may be undertaken only through these registered entities.

• International organisations may be involved for designing, monitoring and evaluation of CSR projects.

• Chief Financial Officer or Finance Head of the Company has to certify that the CSR funds have been utilised for the same purpose as approved by the Board of Directors of the Company.

• CSR Committee to formulate a detailed annual action plan covering CSR projects/programs, manner of execution, modalities of utilisation of funds, implementation schedule, monitoring and reporting mechanism etc.

• Undertaking of impact assessment through an independent agency is made mandatory for Companies having an average CSR obligation of ₹ 10 Cr. or more in three immediately preceding financial years;

• Mandatory disclosure of the composition of CSR committee, CSR Policy, Projects approved by the Board on Company’s website.

• CSR Reporting in Director’s Report to be done in a revised format for the financial year commencing on or after 1 April 2020.

• CSR amount may be spent by a Company for creation or acquisition of capital asset which shall be held by the following entities:

– a company established under section 8 of the Act, or a Registered Public Trust or Registered Society, having charitable objects and CSR Registration Number – beneficiaries of the said CSR project, in the form of self – help groups, collectives, entities; or a public authority

4. MCA has vide General Circular No.01/2021 dated 13 January 2021, has clarified that spending of CSR funds towards awareness campaigns/programmes or public outreach campaigns on COVID-19 vaccination would be an eligible CSR activity

General Meetings:

1. MCA has vide General Circular No.39/2020 dated 31 December 2020, has granted a further extension to conduct EGMs through VC or OAVM or transact items through postal ballot up-to 30 June 2021.

2. MCA has vide General Circular No.02/2021 dated 13 January 2021, enabled the companies whose AGMs were due to be held in the year 2020 or become due in the year 2021 to conduct their AGM on or before 31st December 2021 through VC

Direct Tax

Circulars/Notifications/Press Release

CBDT: Fund managers remunerated at arm's length - sufficient compliance u/s. 9A for FYs 2019-20 & 2020-21; Relaxes Rule 10V condition

CIRCULAR NO. 1 OF 2021 [F. NO. 370142/2/2021-TPL

• CBDT relaxes the requirement of remunerating fund managers of certain offshore funds in view of amended Rule 10V for availing the special taxation regime u/s. 9A: “for the financial years 2019-20 and 2020- 21 in cases where the remuneration paid to the fund manager is lower than the amount of remuneration prescribed under sub-rule (12) of rule 10V of the Rules but is at arm’s length, it shall be sufficient compliance to clause (m) of sub-section (3) of section 9A of the Act.”

• Takes note of the representations received expressing inability to comply with Rule 10V [amended w.e.f. April 1, 2019, vide CBDT notification 29/2020] regarding the amount of remuneration to be paid by the fund to a fund manager for FY 2019-20 as the said Notification was notified after the financial year got over

• Lastly, makes it clear that the remuneration to be paid to the fund manager for FY 2021- 22, shall be in accordance with Rule 10V(12) and that the application for lower remuneration in terms of 2nd proviso for this year, if any, may be filed not later than 15 February 2021.

Launching of e-portal by CBDT for filing complaints

Press release dated 12 January 2021

• CBDT has launched an e-portal for filing complaints regarding tax evasion/Benami properties/Foreign undisclosed assets.

• This step is taken towards encouraging participation of citizens in curbing tax evasion.

• Public can now file complaint using e-filing portal and there will be a unique number provided to each complaint.

• The complainant will be able to view the status of the complaint on the Department’s website.

The search conducted in Assam by Income-tax Department

Press release dated 12 January 2021

• Income tax department carried out search and survey at 29 locations in Assam.

• And the same are carried out on renowned Doctors/Medical professionals.

• The allegations were that they have grossly understated their medical receipts and turnover.

• Due to the search and survey, Unexplained investments / income / expenses worth of more than ₹ 100 Cr. were found.

Search conducted in Hyderabad by Income tax Department

Press release dated 12 January 2021

• Income tax department carried out a search and survey in Hyderabad.

• The search carried out on a prominent civil contractor generating cash using bogus subcontracts and bogus billers.

• The search has also covered a network of individuals running the racket of entry operation and generation of huge cash through fake billing.

• So far, documents evidencing accommodation entries of more than ₹ 160 Cr. have been found and seized.

Search conducted in Kolkata by Income tax Department

Press release dated 08 January 2021

• Income tax department carried out search and survey in Kolkata on real estate and stockbroking groups.

• The search is based on the available data in the departmental database, analysis of their financial statements, on market intelligence and field enquiries.

• So far, the unaccounted cash worth of ₹ 3.02 Cr. and jewellery worth of ₹ 72 L were found in search and survey.

IT department conducts searches in Jaipur

21 January 2021

• The Income Tax Department carried out search and survey operations on 19 January 2021 in Jaipur on one jeweller and two real-estate colonizers and developers.

• During the search, a plethora of incriminating documents and digital data in the form of unaccounted receipts, unexplained development expenses, unexplained assets, undisclosed incomes, cash loans & advances, on-money receipts, benami property, etc were found from hidden basements and cavities in the main premises of these groups.

• In all, unaccounted & unrecorded transactions exceeding ₹1400 Cr. have been unearthed due to the search & seizure operation conducted on these 3 groups.

• The search operations are continuing, and further investigations are under progress.

IT department conducts searches in Pune

21 January 2021

• The Income Tax Department carried out search and survey operations on 12 January 2021 in the cases of leading builders located in Borivali-Mira Road-Bhayander Area of Thane.

• The search action has resulted in the seizure of unaccounted cash of ₹ 10.16 Cr. and unaccounted income of earlier years amounting to ₹520.56 Cr. was detected.

• Further, the unrecognized sales revenue of ₹ 514.84 Cr. for FY 2019-20 has been accepted by the group during the search action and the group has agreed to pay Self Assessment Tax on the same.

CIT vs GE India Technology Centre Private Limited, Karnataka HC, ITA No 282 of 2013

• Karnataka HC dismisses Revenue’s appeal, confirms Tribunal’s deletion of TP-adjustment on account of interest on External Commercial Borrowings (ECBs) paid to the AEs

• In case of GE India Technology Centre (assessee) for AY 2006-07; Assessee had obtained 2 ECBs at the interest rates of 7.5% and 8.49% respectively, however, the TPO recomputed and scaled the interest rate down to 5.67%;

• HC notes that RBI has given the approval in respect of rate of interest on the ECBs obtained by the assessee and observes that “approval given by the RBI with regard to the rate of interest is a relevant factor while the determination of rate of interest”.

• Also observes that “… the rate of interest should be determined on the basis of rate of interest prevailing at the time of availing the loan”

• Further, noting that the rate of interest has been accepted by the AO for the AYs 2002-03 to 2008-09 except for the impugned year i.e., AY 2006-07, affirms ITAT’s observation that “Revenue cannot be allowed to make a departure in case of rate of interest for AY 2006-07”, refers to SC ruling in Radhasoami Satsang

ITAT: Interprets Sec. 240; Sets-off disputed carried forward loss, pending under remanded assessment, in succeeding AYs

Shelf Drill J T Angel Limited vs DCIT(IT), Mumbai, ITA No. 1889 and 1891/Mum/2020, dated 05 January 2021

• Mumbai ITAT allows set-off of business loss in AY 2016-17 and 2017-18, pertaining to AY 2014-15, despite the pendency of de novo assessment remanded by ITAT, but clarifies that it “should not be construed as our direction for the grant of refund…”

• Assessee, resident of Cayman Islands, engaged in providing drilling services for exploration and production of mineral oil furnished business loss of ₹ 80 Cr. which was disallowed by Revenue and remanded by ITAT for de novo consideration;

• Revenue denied the set-off of business loss carried forward from AY 2014-15 due to pending assessment proceedings;

• Holds that during the pendency of assessment on remand, assuming that loss was incorrectly determined for AY 2014-15 is premature and uncalled for

• Holds that refund of taxes for the subject AYs could await finalization of assessment for AY 2014-15;

• However, directs Revenue to allow set-off of losses and exercise discretion for granting refund since remanded assessment are to be finalized within three months.

Tirupati Procon Pvt Ltd vs Income-Tax Officer dated 14 January 2021 [ITA No. 8224/DEL/2019]

• The assessee has filed a return declaring zero income and the same is been selected for scrutiny.

• AO noticed that the assessee had shown interest expense during the year, hence asked for the loan agreement/sanction of loan and other relevant documentary evidence to prove the genuineness of the interest.

• Assessee had submitted respective lender’s ledger, however told that it is taken on mutual terms, therefore there is no documentary evidence.

• AO also noticed that there was interest credited in the books however no actual bank payment is made and there is no unsecured loan was received by the assessee in the year under appeal.

• AO issued notice to the lender to get the information under section 133(6) of the IT Act, however there was no reply received.

• The assessee provided a detailed reply to the AO that part of the loan taken had been invested in the company for business purpose. Also, it is keeping books on mercantile basis, hence actual interest payable or paid should not be the matter for taking allowance.

• He also requested that in case both of the parties not responded to the notice of AO, AO should summon them under section 133 of the act.

• AO did not accept the contention of the assessee and noted that assessee could not prove the terms of the loan and only the verbal agreement can not be sufficient to claim and hence disallowed the interest expense under section 37(1).

• Assessee challenged it before LD. CIT(A).CIT(A) dismissed the contention of the assessee and directed the AO to take remedial action against the lender for obtaining the loans.

• LD counsel of the assessee submitted that the loans taken in the earlier years and allowed interest in the earlier years, also had shown the ledgers and confirmation from the lender taken in the earlier years. And, since there was no appeal is pending of preceding year in which the loan was taken , there should be no need to take remedial actions for that.

• Taking the help of the case of CIT vs. Sri Dev Enterprises 192 ITR 165, he concluded that the Income-tax authorities shall follow the rule of consistency and definiteness of approach in dealing the matter. In the earlier years, the loan was there in the books and interest was paid on that, that time it was not a case of dispute and now also it should on not be.

HC: Uttarakhand HC directs CBDT to leniently view consequences of late-filing of tax-audit, returns

Dehradun Chartered Accountants Society V/s Department of Revenue

• Uttarakhand HC disposes off Dehradun Chartered Accountants Society’s (petitioner) writ petition on lines similar to Gujarat HC decision which had declined to interfere on tax audit, return filing due-dates extension

• While Gujarat HC had issued directions to CBDT to leniently view the consequences of late-filing arising from Sec 271B, petitioner herein submits that , there are other provisions which equally have consequences flowing in case the Income Tax Returns are not filed on time

• HC permits the petitioner to submit a fresh representation before CBDT, voicing all their grievances, with regard to the consequences which would flow from different provisions of the Act

• Accordingly, directs CBDT to leniently consider the said representation after giving an opportunity of hearing to the petitioner

ITAT: Sec 50C amendment prescribing 'tolerance limit' while adopting stamp duty valuation, retrospective in nature

Maria Fernandes Cheryl V/s Income Tax Officer ITA No. 4850/Mum/2019

• Revenue had held that the tolerance limit envisaged in the proviso to Sec.50C was applicable prospectively and declined to ignore the variation of 6.55% between sale consideration declared by assessee and the stamp duty value;

• Rejects Revenue’s submission that the amendments can only be prospective in nature as the law states so specifically, refers to Delhi HC ruling in Ansal Landmark Township holding that a curative amendment is to be treated as retrospective in nature even though it may not state so specifically;

• ITAT explains that the rigour of Sec.50C(1) was relaxed to take bonafide cases of small variations between sale consideration vis-à-vis stamp duty valuation attributable to various factors such as location of property, near-by public amenities, size of land and building out of the scope of adjustments u/s 50C,

• Thus opines that the amendment is a curative one to take care of unintended consequences of Sec.50C; States that “….just because there is a small variation between the stated sale consideration of a property and stamp duty valuation of the same property, one cannot proceed to draw an inference against the assessee….this insertion of the third proviso to Section 50C(1) is in the nature of a remedial measure….”;

• Explaining the reason for insertion of third proviso to Sec.50C, holds that “Once legislature very graciously accepts, by introducing the legal amendments in question, that there were lacunas in the provisions of Section 50C…..there is no escape from holding that these amendments are effective with effect from the date on which the related provision, i.e., Section 50C, itself was introduced.

ITAT: Limitation u/s 154 runs from the date of assessment order for an issue not appealed against

Karnataka Power Corporation Ltd. Vs ACIT, ITA No.282/Bang/2017

• Bangalore ITAT dismisses the suo moto rectification by Revenue, of the issue not raised in the appellate proceedings for AY 2002-03, holds it time-barred u/s 154(7); Revenue calculated the period of limitation from the date of order passed after ITAT’s remand order instead of the date of assessment order initially passed by applying the doctrine of merger

• ITAT rejects the applicability of the doctrine of merger by relying upon SC ruling in Alagendran Finance Ltd. where it was held “..doctrine of merger applies only in respect of such items which were the subject matter of appeal and not which were not…”

• Also relies upon Karnataka HC ruling in Kothari Industrial Corporation Limited to explain that if the matter of the dispute is same in two rectification orders passed then the period of limitation would be calculated from the date of first rectification, otherwise the date of original assessment order would need to be considered

Bombay HC: Directs Revenue to withdraw the appeal, considers assessee’s settlement of tax payable under VsVS

• The Assessee, Chempsec Chemicals P. Ltd., had opted for settlement under Direct Tax Vivad se Vishwas Act, 2020 (“VsV Act”) for AYs 1988-89, 1999-00, 2000-01, 2001-02 and filed declaration for the same under VsV Act. The designated authority issued certificates under VsV Act and these amounts were paid by the assessee on 23.12.2020.

• However, for passing of final order, any pending appeal for the Assessment years is required to be withdrawn. The VsV Act and the clarifications of CBDT via circular No. 7 /2020, is silent regarding withdrawal of appeal by the income tax department.

• However, from the answers given to question Nos. 21 and 48 of the above circular and based on the intent of the VsV Act for settlement of pending disputes, the HC ruled in favor of the Assessee.

• The HC held that if the assessee has paid the said amount of tax and the same is accepted by the designated authority, it would be unjust to allow an appeal under such a case and thus, the income tax department would be under an obligation to withdraw the appeal.

Bangalore ITAT: Limit u/s 154 runs from the date of assessment order for an issue not appealed against

Karnataka Power Corporation Ltd. Vs ACIT, [ITA No. 282 /Bang/2017], 21 January 2021

• The Assessee is a power generation company which was assessed u/s 143(3) on February 19, 2005 for AY 2002-03 which was revised by CIT(A) by making certain disallowances of capital expenditure. On an appeal by the assessee, ITAT remanded a specific matter back to the CIT(A). On October 10, 2011 an assessment order was passed against the assessee and the assessee appealed with the CIT(A). During the pendency of original appeal, Revenue passed a rectification order u/s 154 on March 28, 2012 after realizing its own mistake, apparent from record, and disallowed the deduction u/s 80IA.

• Being aggrieved by the rectification order, which reduced the brought forward loss of ₹ 80.55 crores, assessee approached CIT(A) with a plea of limitation against the rectification order under section 154 of the act to 4 years of the order. CIT(A) upheld the rectification order.

• ITAT held that as per the doctrine of merger, two appeals cannot be merged unless their subject matters are same/similar. Further, based on Karnataka HC ruling in case of M/s Kothari Industrial Corporation Limited, where it was held that “period of limitation for a second rectification should be reckoned from the date of original order, if subject matter of second rectification is different from subject matter of the first rectification” , the Bangalore ITAT held that rectification order dated 28.03.2012 would be barred by limitation u/s 154(7) against the original assessment order dated 10.02.2005.

Barclays Technology Centre India Pvt Ltd vs DCIT, [ITA No. 601 /PUNE/2017], 27 January 2021

• Pune ITAT deletes disallowance u/s 40(a)(ia) for TDS non-deduction u/s 194J on leased line charges paid by Assessee-company during AY 2012-13;

• Acknowledges that the leased line charges paid by the Assessee was in the nature of `Royalty’ under the terms of Explanation 6 to Sec.9(1)(vi), inserted by the Finance Act, 2012 w.r.e.f. 1 June 1976;

• However noting that the Finance Act, 2012 was enacted somewhere after the close of the F.Y. 2011-12 (i.e. AY 2012-13), explains that the liability to deduct tax at source can be fastened only under the law prevailing at the time of payment and if no liability exists at the time of payment, any subsequent retrospective amendment cannot be enforced against the payer; Remarks that “even though the amount became chargeable to tax as royalty in the hands of the recipient the same did not fasten an obligation to deduct tax at source as the Assessee could not have activated its sixth sense to ascertain beforehand that an obligation to deduct tax at source was in offing.”; Rules that as the scope of “Royalty” came to be expanded after the close of the financial year, the same could not have triggered disallowance u/s.40(a)(ia);

• Further, on the disallowance of expenditure on purchase of RSA tokens, accepts Assessee’s submission that the amount repaid by its AE at cost plus 15% was considered as part of income and deletes the disallowance; Holds that “Once the amount of expenditure, debited to the Profit and loss account, gets specifically credited to the Profit and loss account with a certain mark-up, there can be no question of disallowing the expenditure so charged while continuing to treat the amount credited as income.”

ITAT: Holds set-off of loss from sub-lease 'business' against 'house property income' from sub-leasing, allowable

Prolific Consultancy Services (Mumbai) Pvt Ltd vs ITO Ward 8(2), ITA No. 2731, 2732 and 2733/MUM/2013

• Mumbai ITAT rules that the routine and mandatory expenses incurred by assessee co. (engaged in acquiring property on lease and sub-leasing) for maintaining its corporate identity would be eligible as regular business loss, allows consequential set off of the same with house property income arising from subletting.

• Following the co-ordinate bench ruling in assessee’s own case in earlier years, the assessee had offered income from sub-lease of property under the head ‘income from house property’ during subject AYs 2013-14 & 2014-15

• ITAT takes note of the nature of assessee’s business, being taking property on lease and sub-leasing the same and derive rental income thereon

• ITAT opines that “The rental income derived out of sub-leasing activity may get taxed under the head ‘income from house property’ as per certain provisions of the Act and judicial precedents. But it cannot be denied that the assessee had indeed carried on its business of sub-leasing the property.

• Thus, holds assessee would be eligible for set off of the same with the house property income

• The ruling was delivered by the Mumbai Bench of ITAT comprising Shri M. Balaganesh and Shri Ravish Sood.

ITAT: No addition u/s 68 for assessee opting for presumptive taxation u/s 44AD

Dinesh Kumar Verma Vs ITO Ward 2(1), ITA No. 1183/MUM/2019

• Mumbai ITAT deletes Sec.68 made for Assessee-individual during AY 2014-15, holds that Sec.68 cannot be invoked where the Assessee has filed return of income u/s 44AD without maintaining books of accounts.

• Revenue had made additions u/s 68 w.r.t Assessee ’s cash deposit into his bank account treating as unexplained cash.

• Perusing Sec.68, ITAT states that the section “makes explicitly clear that the addition can be made under the section if, any sum is found credited in the books maintained by the Assessee”

• Rejects Revenue’s contention that passbook of Assessee ’s bank account constitutes books of account

• Opines that “Since section 44AD does not obligates the Assessee to maintain books, the provisions of section 68 cannot be invoked where the Assessee has filed return of income under the provisions of section 44AD.”

Other updates/News

IT Dept. assures no late fee u/s 234F; Updated ITR filing utility incorporating due-date extension soon

Twitter dated 01 January 2021

• IT Dept. assures that no late fees will be calculated by CPC while processing the returns filed before the updated ITR filing utility is deployed;

• Updates that “The changes as a result of due date extension will be made available shortly.”

CBDT: Issues Protocol for handling breach of information exchanged under tax treaties

Dated 06 January 2021

• Foreign Tax & Tax Research Division of CBDT has circulated a Breach Protocol prepared as per the international standards and approved by Information Security Committee (ISC) to all the offices of Income Tax Department (ITD) handling information exchanged under a treaty

• The Protocol shall get triggered in the event of an incident of inappropriate access, disclosure, use of confidential information, or failure to safeguard data

• The Protocol details a three-step approach to handle a breach:

(i) ‘Governance of a Breach’ that highlights the precautions to be taken and the evidence to be collected prior to activation of breach protocol by ISC,

(ii) ‘Breach Management’ that involves identifying the source of the breach viz., internal or external, containing the immediate impact of the breach by removing the attackers access to the system, eradicating the key component of the risk and mitigating the vulnerabilities that were exploited, and taking remedial actions to ensure that adequate security measures are instituted so as to prevent security incidents of similar nature, and

(iii) ‘Communication Protocol’ that lays down the course of communication to be undertake in the event of a breach.

CBDT assigns all penalty cases to National Faceless Penalty Centre except in 3 cases

Order, dated 20 January 2021

• In exercise of power conferred under para 3 of the Faceless Penalty Scheme, 2021, the Central Board of Direct Taxes (CBDT) has directed that all the penalty cases, pending as well initiated subsequently, is assigned to the National Faceless Penalty Centre to be disposed of by the National Faceless Assessment Centre (NeAC) in accordance with Faceless Penalty Scheme 2021.

• However, penalty proceedings under the following circumstances shall not be subject to faceless penalty scheme:

a) Penalty proceedings in cases assigned to Central Charges

b) Penalty proceedings in cases assigned to International Tax Charges; and

c) Penalty proceedings arising in TDS Charges.

INDIRECT TAX

CAG cannot audit private entities, says Bombay High Court

Under the erstwhile Indirect tax regime (before GST), large business entities would receive notice for Central Excise Revenue Audit (CERA) of their central excise and service tax compliances. This audit is conducted under the overall supervision of the Principal Director of Audit, (Central) Kolkata in the Indian Audit Department of Government of India. CERA audit traces its power under the provisions of Section 16 of the Comptroller and Auditor General’s (Duties, Powers and Conditions of Service), Act 1971. Now, Bombay High Court in a writ petition filed by M/s Kiran Gems Private Limited has held that CAG cannot perform CER audit of private entities. Hon’ble High Court in this case discussed at length relevant articles of Constitution of India which deals with duties and powers of CAG as well as provisions of the said Act which deal with the audit. The Court observed that the power of the CAG extends to any office or the department of the Government and cannot be construed to extend to a private entity. Further in exceptional cases, with the prior approval of the President of India or the Governor of the State, CAG can audit the accounts of any body or authority, which undertakes the functions of the Government. In the present case, the writ Applicant had received notice for CER audit both for period pre- and post-GST under the provisions of Section 16 of the Comptroller and Auditor General’s (Duties, Powers and Conditions of Service), Act 1971. Having regard to the scheme of the said Act, High Court held that the department’s action is wholly without jurisdiction and constitutional.

Goods and Services Tax

No input tax credit on marketing/promotional materials provided free of cost to customers

Haryana Authority for Advance Ruling (AAR) in the case of M/s BMW India Pvt Ltd (Applicant) has held that input tax credit is not eligible in respect of branded lifestyle goods provided free of cost during promotional/marketing events to existing and prospective customers. The facts, in this case, are that the Applicant BMW India organizes various events across the year for the purpose of marketing and sales promotion of its products such as motor cars, motorbikes bearing BMW brands. Such events are organized throughout the country with an intention to increase the brand loyalty of its customers. These events also aid as a platform to undertake advertisement, sales promotional activities for its existing/potential customers. During the course of these events, the potential customers are identified and are offered test drives of BMW cars, leading to follow-ups and eventually resulting in the sale of BMW cars, while the existing customers are provided with exchange offers etc. During these events, the attendees are provided various BMW branded lifestyle products such as Duffle bags, Golf balls, T-shirts, Caps, Diary, Keychain, Passport holder etc. on a free of cost basis.

The Applicant, in this case, contended that a clear distinction should be drawn between goods given as a ‘gift’ and goods are given on ‘free of cost’ basis. According to the Applicant, they organize such marketing events with a sole intent of enhancing the loyalty of its existing customers and attracting potential customers which ultimately helps in increasing the sale of BMW products in India. Thus, the supply of promotional materials free of cost is in the course or furtherance of its business and not as a gift. Thus, they are eligible to avail input tax credit on these promotional materials.

AAR, on perusal of definition of ‘consideration’ under the Central GST Act, 2017, rejected the Applicant’s contention that the goods supplied by it in the marketing events are intended to earn consideration in the form of reciprocity from customers and increase in sales and brand value of the company. AAR in this regard noted that, it is true that the existing BMW customers must have paid some consideration at the time of purchasing BMW motor cars/ motorbikes but this consideration was in a respect of the supply of motor cars or motorbikes. This consideration does not have the remotest connection with the goods supplied on free of cost basis in the promotional events. Further, as far as the supply of goods to the potential customers is concerned, AAR observed that the issue of consideration does not arise because the potential customers may not be actual customers. Thus, there is no consideration involved at the time of making these free of cost supplies. Finally, AAR concluded that items distributed in the promotional events are ‘gifts’ and in terms of Section 17(5)(h) of the Central GST Act, 2017, the Applicant is not eligible to claim the input tax credit on promotional materials.

Eligibility to input tax credit on promotional materials/brand reminders provided FOC - no advance ruling due to divergent views among AAAR members

In another similar case in M/s Sanofi India Limited (Applicant), interestingly, members of the Appellate Authority for Advance Ruling (AAAR) had divergent views and consequently, no ruling was given by the AAAR on the question posed by the Applicant.

Brief facts involved in this case are the Applicant is engaged in the business of sale of pharmaceutical goods and services. In the regular course of business, they incur various marketing and distribution expenses to promote their brand/products and enhance sales. This involves the distribution of promotional items/brand reminders. Further, the Applicant also offers various promotion schemes such as “Shubh Labh Trade loyalty Program” etc. In case of brand reminders, products like pen, notepad, keychains etc. are provided to distributors with Applicant’s name embossed on it. In the case of “Shubh Labh Trade Loyalty Program”, the distributors/wholesalers earn reward points basis the quantity of goods sold by them. These reward points can later be redeemed for foreign tours, branded merchandise etc. The merchandise is purchased by the Applicant in its own name and provided to distributor/wholesales free of cost. The question that the Applicant had posed is whether they are eligible for an input tax credit of GST paid on the expenses of the said promotional schemes, brand reminders etc. The Authority for Advance Ruling (AAR) had held that the Applicant is not eligible for an input tax credit in this case. The Applicant then preferred an appeal before AAAR against this AAR Ruling.

Both the Member (CGST) and the Member (SGST) perused various provisions of the GST law viz. definition of ‘inputs’, input services’, the scope of the term ‘supply’, the scope of Section 16 (eligibility and conditions for taking input tax credit), Section 17 (blocked credits) etc as well as various Court Rulings relevant to this case.

Member CGST held in favour of the Applicant that they are eligible to take the input tax credit in the present case. Member CGST noted that the brand reminders fulfil the advertisement need of the Applicant and its product. These are provided with an implicit commercial motive of growth in the sale of products with the aid of distributors and these are not in the nature of ‘gift’. Further, under the promotional schemes such as ‘Shubh Labh Trade Loyalty Program’, the Applicant do not provide promotional goods and services to each and every distributor but only to such participating distributors who have achieved their sales target and accumulated reward points. Thus, there is a pure commercial intention on the part of the Applicant to increase their business and sales.

On the other hand, Member SGST held against the Applicant that they are not eligible for an input tax credit in this case. Member SGST noted that goods and services provided by the Applicant to the distributors both under the promotional scheme ‘Shubh Labh Trade Loyalty Program’ and as brand reminders are free of cost and there is no consideration received by the Applicant. Thus, once it is established that the subject goods/services are provided free of cost and there is no contractual obligation against the supply of such brand promotional goods, the only conclusion that can be drawn is that these are given as gifts by the Applicant to the distributors. Member SGST also noted that there is no doubt that the brand reminder goods with the Applicant’s name embossed on it has advertising potential and it is in the furtherance of business, but since Section 17(5) dealing with blocked credits starts with a non-obstante clause, it overrides Section 16(1) of the CGST Act. As the legislature has denied input tax credit under Section 17(5)(h) on such goods, the Applicant is not eligible to claim an input tax credit in the present case.

18% GST leviable on notice pay recovery from employees

Gujarat Authority for Advance Ruling (AAR) in the case of M/s Amneal Pharmaceuticals Pvt Ltd (Applicant) held that the Applicant is liable to pay 18% GST on the recovery of notice pay from the employees who are leaving the company without completing the notice period as specified in the Appointment Letter. AAR, in this case, perused the Appointment Letter issued to employees and observed that if any employee does not serve the notice period after tendering his resignation, then as per the Appointment Letter, the Applicant is entitled to recover the notice pay from the agreed portion of salary to compensate the loss to the Applicant. Further, the notice pay is nothing but the amount stipulated in the employment contract for not serving the stipulated notice period. In other words, notice pay is a sum mutually agreed between the employer and the employee for breach of contract. It can be regarded as a consideration to the employer for “tolerating the act” of the employee to not serve the notice period, which was the employee’s agreed contractual obligation. This would mean that the employee while accepting the offer of employment, has not only understood the intent on the part of the employer in prescribing this exit condition but has also accepted it. Thus, AAR ruled that this transaction of the employer agreeing to the obligation of tolerating an act (quitting without any advance notice) on the part of the employee, for payment of a sum (notice pay), will be covered under clause 5(e) to Schedule II to CGST Act 2017, as a declared service taxable at 18%.

Liaison office not liable to pay GST on reimbursement received from head office

The Authority for Advance Ruling (AAR) in the case of M/s WILHELM FRICKE SE held that liaison office is not liable to pay GST and is also not required to obtain GST registration. The AAR observed that the liaison office is strictly prohibited to undertake any activity of trading, commercial or industrial nature and cannot enter into any business contracts in its own name. Liaison office does not earn any commission, fees or remuneration for the liaison activities/services rendered by it. Liaison office does not have any other source of income and it is solely dependent on the HO for all the expenses incurred by them such as payment of salary to employees, reimbursement of expenses towards rent, electricity, security, travelling etc. Therefore, the HO and liaison office cannot be treated as separate persons. Consequently, there cannot be any flow of services between them as one cannot provide service to self and therefore, the reimbursement of expenses made by the HO cannot be treated as consideration towards any service.

Remuneration to Director declared as fees for professional or technical services liable to GST under RCM

Rajasthan Appellate Authority for Advance Ruling (AAAR) in case of M/s Clay Craft (India) Pvt Ltd has held that remuneration paid to independent Directors and that part of employee Director’s remuneration which is declared as fees for professional or technical services and subject to TDS under Section 194J of the Income Tax Act, is taxable under GST law and the Company is liable to pay GST under reverse charge mechanism. AAAR also ruled that Director’s remuneration declared as salaries in Books and subjected to TDS under Section 192 of the Income Tax Act is not taxable under GST law being consideration for services rendered by an employee to the employer which is outside the purview of GST law. This Ruling from Appellate Authority modifies the earlier ruling of Rajasthan AAR which had held that Director’s remuneration is liable to GST under RCM without appreciating the employer-employee relationship.

No input tax credit on canteen services to employees though mandated under Factories Act

Before we begin discussing this Ruling, let us understand legal background behind this issue. Section 17(5) of the CGST Act, 2017 deals with blocked input tax credits which means input tax credit in respect of specified goods and services is not allowed. Clause (b) of Section 17(5) has three items from (i) to (iii) which inter alia deals with food and beverages, outdoor catering, employee insurance, club/fitness center membership, travel benefits to employees etc. With effect from 1 February 2019, a proviso was inserted in clause (b) of Section 17(5) to provide that if it is obligatory for an employer under any law to provide the subject goods/services to employees, then input tax credit would be eligible. Interesting to note here is that this proviso is inserted after item (iii) of clause (b) in Section 17(5) whereas food and beverages, outdoor catering is included in item (i).

The Authority for Advance Ruling (AAR) in case of M/s Musashi Auto Parts Pvt. Ltd. (Applicant) has held that even though it is mandatory under the Factories Act to provide meals to the employees, the Applicant is not eligible to claim input tax credit of GST paid on canteen services availed from contractors. While arriving at this conclusion, AAR noted that the newly inserted proviso is with regard to the provision contained in item (iii) of clause (b) of Section 17(5) (which deals with travel benefits extended to employees) and the same ought not to be read with item (i) which deals with food and beverages and outdoor catering. Consequently, AAR denied credit to the Applicant on canteen services.

Who is recipient of service in case of post-sales support services?

The facts in this case are that M/s Stovec Industries Ltd, Gujarat (Applicant) is a subsidiary in India of M/s SPG Prints Austria GMBH (SPA). Applicant has entered into a contract with SPA to provide certain services to customers of SPA in India, as per SPA’s instructions. Such services include installation/up-gradation of machines sold by SPA, training at SPA’s customers’ site etc. Applicant raises invoice on SPA for such services and receives payment in foreign currency. One of the questions that Applicant posed before AAR is whether service recipient in this case is SPA or the customers of SPA, located in India? This question is particularly relevant to determine whether services of the Applicant would be classified as export of services and thus, exempt or otherwise.

The Gujarat Authority for Advance Ruling (AAR) in this case has held that the customers in India of SPA would be indeed service recipients. In arriving at this conclusion, AAR analyzed the relevant definition of service recipient under CGST Act, 2017 and observed that the ‘recipient’ is so defined under CGST Act as to make separation impossible between the person to whom the supply is made and the one liable to pay the consideration. AAR further ruled that services of Applicant cannot be categorized as export of services under GST law.

No GST on electricity charges reimbursed by tenant to landlord

The Gujarat AAR in the case of M/s Gujarat Narmada Valley Fertilizers & Chemicals Ltd. has held that electricity charges collected by landlord from tenant along with lease rentals would not form part of value of supply of rentals and thus, GST is not applicable on the said charges. While arriving at this conclusion, AAR perused various clauses of the lease agreement and observed that electricity charges collected by landlord are at actuals based on reading of sub-meters. Thus the landlord in this case acts in the capacity of ‘pure agent’ as per Rule 33 of the Central GST Rules.

DG set consumption charges recovered by landlord taxable at 18%

The Haryana AAR has held that facility of arranging power back-up in a commercial or residential building is a supply of ‘property management service’ and not a ‘supply of electrical energy’ and hence, the same is taxable at 18%. The Applicant in this case M/s Pansut Udyog Pvt Ltd renders facility management services to an IT/ITeS building in Gurugram, Haryana. They have installed diesel generators at its tower to facilitate power back-up. Applicant recovers DG set consumption charges at actuals from tenants based on reading of separate meters installed and applicant does not make any profit out of this. Applicant contented that, diesel generator is a device that converts mechanical energy obtained from HSD into Electrical energy. Considering the fact that, electricity energy attracts NIL rate of GST, they are not liable to pay tax. However, AAR rejected the contention of the Applicant by stating that Applicant is neither an electricity generating nor an electricity distribution agency. They merely provide power-back services in the said building which is in the form of a service, taxable at 18%.

Advance money forfeited with respect to sale of land, liable to GST 18%

The Gujarat AAR in the case of M/s Fastrack Deal Comm Pvt. Ltd. has held that amount forfeited as a result of breach of sale agreement of land is covered under supply of service as per clause 5(e) of Schedule II of CGST Act, 2017 and therefore, liable to GST.

The AAR elucidated that forfeiture amount is not received on account of sale of land but received on account of non-fulfillment of conditions of the agreement by the customer. The amount so received would be termed as a consideration for “refraining or tolerating or doing an act” of the customer to not complete the transaction, which the customer had agreed in terms of contractual obligations.

Booking of plots amounts to sale of land, but development of the said property taxable at 18%

The Haryana AAR in the case of M/s Informage Realty Pvt Ltd, has held that booking of / sale of developed plots whether before or after completion of the development work, amounts to ‘sale of land’ and hence not leviable to GST. However, sharing of land by the landowners with the developer against certain development services (discussed in next para) to be provided by the developer would be a consideration for supply of works contract services by such developer and hence, attract GST at 18% to be paid by Applicant-developer.

In the given case, the developers and the landowners proposed to enter into an agreement to develop the land into a residential plotted township/colony. As per the agreement, the landowners agreed to give 20% of the licensed plotted area to applicant as consideration for doing following activities:

a. Applying and obtaining license to develop the land using its technical and financial capability;

b. Development of residential plotted colony;

c.Laying of roads, sewerage, storm water system, providing electricity poles etc.

The AAR noted that the nature of the agreement between the parties is of a JDA and contains two kinds of transactions. One pertains to booking/selling of plots and the other being transfer of 20% share of developed land/plots by each of the landowners to the developer.

Accordingly, AAR held that the first transaction of booking / sale of developed plots amounts to ‘sale of land’ on which no GST is payable. For second part of the transaction of transferring 20% share of plots by the landowners to the developer, it held that such transfer is a consideration for the services to be rendered by the developer to the landowners. The transfer value of the plots would be considered as consideration paid by the landowners for the services rendered by the Applicant for development of the land which would be taxable as ‘works contract services’ at 18%.

Customs Update

SEZ units to mention intention to avail RoDTEP benefit in ‘remarks’ column of shipping bill

Department of Commerce has issued an Advisory to all SEZ units for availing benefit under the Remission of Duties and Taxes on Exported Products (RoDTEP) scheme which is introduced from 1 January 2021. As per the Advisory, SEZ units need to mention the following in the remarks column of shipping bill:

“Shipping bill filed under RoDTEP Scheme if applicable to SEZ Units and subject to such conditions as prescribed including the product coverage”.

Customs litigation update

Bombay High Court issues direction to department to reassess bills of entry to correct the inadvertent error made by the importer in bill of entry

The Facts, in this case, are that the importer M/s Dimension Data India Pvt Ltd filed five bills of entry for clearance of imported goods viz. routers for home consumption. Due to typographical error in mentioning tariff code in bills of entry, importer ended up paying 20% customs duty whereas the actual rate of duty was Nil. This cost importer ₹14.5 crores as import duty. On realizing this mistake in internal audit, importer filed an application with the customs department for a reassessment of bills of entry to correct this error but could not succeed. The importer then filed a writ petition before Bombay High Court to issue a direction to the department to reassess bill of entry under Section 17(4) of the Customs Act.

Customs department argued before High Court that under the self-assessment scheme, the burden is on the importer to ensure correct classification and rate of duty on goods. As, in the present case, the process of import is already complete, importer ought to challenge his self-assessment by filing an appeal before Commissioner (Appeals).

High Court perused the provisions of the Customs Act and noted that though the duty is cast upon an importer to self-assess the customs duty, a corresponding duty is also cast upon the proper officer to verify and examine such self-assessment and officer of customs has the power under Section 17(4) to make re-assessment in case self-assessment done by the importer is not correct. Further, the Court observed that Section 149 and 154 of the Customs Act respectively permit amendment of documents already filed and correction of clerical or arithmetical mistakes in any decision or order which would also include an order of self-assessment post out of charge. Reliance was also placed on the decision of Madras High Court in M/s Hewlett Packard Enterprise India Private Limited in which it was held that in a case of correction of an inadvertent error, the appropriate remedy would be seeking an amendment to the Bill of Entry and not fling of appeal because there is no legal flaw in the order of self-assessment amenable to appeal but only a factual mistake which can be rectified by way of amendment or correction. The High Court finally issued directions to the customs department for correction of the said error in the classification of imported goods.

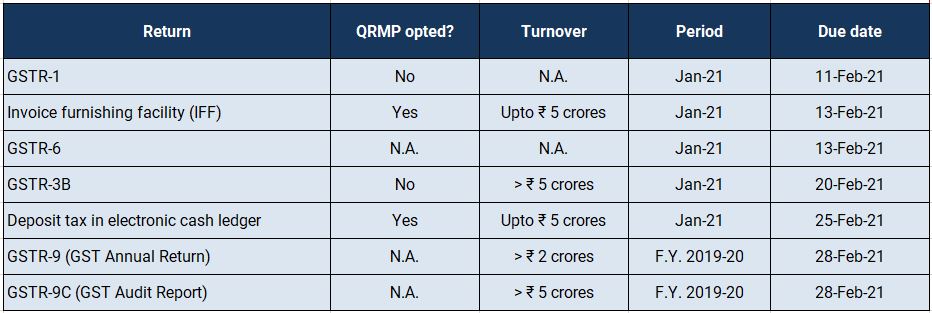

Due Dates

Important Due Dates, February 2021

GST Compliance Calendar

Category 1 States: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

Category 2 States: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi

SINGAPORE UPDATES

Accounting and Corporate Regulatory Authority (ACRA)

1) Register of Registrable Controller (RORC) transaction in BizFile+ to resume in February 2021.

With effect from 30 July 2020, companies and limited liability partnerships (LLPs) were required to lodge RORC information with ACRA via BizFile+ portal, in addition to maintaining their own RORC.

However, the RORC filing transaction in BizFile+ was suspended in September 2020 and will remain suspended until January 2021. The transaction is scheduled to resume in February 2021. Companies and LLPs will be given time up to 30 June 2021 to lodge the RORC information with ACRA.

The Payment Services Act came into force in January 2020. It was released on 4th January 2021 that the Payment Services Act will be read for a second time to make further changes to keep up with evolving innovation and technology, and emergence of new business models in the payment services space.

Enhancing the Regulatory Framework for Virtual Asset Service Providers

The revised Payment Services Act will be expanded to regulated service providers of Digital Payment Tokens (“DPTs”) that facilitate the use of DPTs for payments and may not possess the moneys or DPTs involved. They are sometimes also referred to as Virtual Assets Service Providers. The revised Payment Services Act, in relation to Virtual Assets Services Providers, will regulate the payment service providers who facilitate the transmission of DPTs from one account to another, provide custodial services for DPTs, facilitating the exchange of DPTs where the service provider does not come into possession of the moneys or DPTs involved.

Virtual Assets Service Provider activities are inherently more vulnerable to money laundering and terrorism financing risks due to their speed, anonymity and cross-border nature and therefore becomes critical to be regulated for money laundering and terrorism financing risks. As such, Virtual Assets Service Providers will be required to be licensed under the Payment Services Act and be subject to anti-money laundering / countering the financing of terrorism regulations.

Mitigating Money Laundering and Terrorism Financing Risks

The revised Payment Act will address money laundering and terrorism financing risks and will be expanded wherein the definition of cross-border money transfer service will include facilitating transfers of money between persons in different jurisdictions, where money is not accepted or received by the service provider in Singapore. Therefore, money that does not flow into Singapore will also be caught under the revised Payment Services Act.

Empowering MAS to impose measures on Digital Payment Token service providers

Other sets of changes to the Payment Services Act will look to impose measures on DPT service providers to ensure better consumer protection and maintain financial stability and safeguard the efficacy of monetary policy. Monetary Authority of Singapore (“MAS”) will impose user protection measures on DPT service providers such as the need to segregate customer assets from own assets. Measures will be accorded to the MAS to impose powers on certain Digital Payment Token service providers where it is in MAS’ new necessary or expedient in the interest of the public or section of the public, the stability of the financial system in Singapore, or the monetary policy of MAS.

The new Payment Services Act will be amended to broaden the scope protect individuals involved in domestic money transfer transaction with financial institutions. Currently only major payment institutions providing services like e-money issuance are required to safeguard customer money. This will be amended to include other classes of licensee as well. The revised Payment Services Act will also require extend the duty of care to provide information to MAS which are not false or misleading to all persons including non-individuals.

The various changes to the Payment Services Act will enable MAS to address greater, newer risks identified in the industry and be inline with global regulatory requirements.

2) Revised Technology Risk Management Guidelines

On 18 January 2021, the Monetary Authority of Singapore (MAS) released a revised Technology Risk Management Guidelines to address an environment of growing usage by financial institutions (FIs) of cloud technologies, application programming interfaces (APIs), and rapid software development methods (such as Agile) – some of which the MAS has also been promoting/enabling in the financial industry.

The latest round of revisions is made in response to the fast-emerging technology as well as heightened cyber threat risks. This may also be seen as timely and necessary against the backdrop of recent cyber-attacks in relation to supply chains, where widely-used network management software has become a target and a victim of such attacks.

The revised Technology Risk Management Guidelines also recognises the burgeoning dependence on third party providers by FIs and sets out the expectation for FIs to exercise stronger oversight of arrangements with third party service providers, to ensure system resilience as well as maintain data confidentiality and integrity.

The revised Guidelines also provide guidance and expectations on the roles and responsibilities of the board of directors and senior management in ensuring effective security controls and risk management practices are applied within the FI’s systems. This means that the board of FIs should include members who are equipped to provide effective oversight of technology and cyber risks and should appoint individuals to roles directly responsible for security within the organisation.

In summary, the Guidelines are helpful in highlighting common areas where cyber security is an issue and the key steps FIs can take to address them. A key takeaway is that this development will impact not only FIs, but their IT service providers as well. The Guidelines make it clear that FIs can no longer focus solely on securing their own systems and must now also manage the potential technology risks of their IT service providers as well.