ECB 2 return for the month of October 2020 to be filed on or before 7 Nov 2020.

Company Law update:

In terms of General Circular No. 36/2020 dated October 20, 2020, requirement of residency in India for a period of at least 182 days by at least one director of every company, shall not be treated as a violation for the year 2020-21.

In terms of Circular No. IBBI/LAD/35/2020 dated October 29, 2020, it is required to provide a copy of the application for initiating corporate insolvency resolution process against a corporate debtor, to the Insolvency and Bankruptcy Board, before filing the same with the Adjudicating Authority (National Company Law Tribunal).

• The Taxation Laws (Amendment) Act, 2019, introduced two new sections, i.e., section 115BAA and section 115BAB to provide that an assessee, being a company, can opt for concessional tax rate regime subject to fulfilment of various conditions.

• On the similar lines, the Finance Act, 2020, has inserted two more sections i.e. section 115BAC and section 115BAD to provide that an assessee, being an Individual, HUF and Co-operative society, can opt for concessional tax rate regime subject to fulfilment of various conditions.

• One of the condition to opt concessional rate of tax under section 115BAA (domestic company 22%), 115BAC(individual and HUF) and 115BAD (cooperative society) is that the additional depreciation and unabsorbed depreciation with respect to additional depreciation shall be deemed to have been given full effect and no further deduction of such allowance/loss will be allowed in subsequent years.

• To provide adjustment on above case, the CBDT amends rule 5 providing to adjust the above allowance/losses to the opening WDV of the block of assets.

• CBDT has also notified adjustment of depreciation or allowance for unabsorbed depreciation, Form ITR-6 and Form 3CD have also been amended to furnish relevant information regarding such adjustments.

• CBDT further introduced rule 21AF and 21AH to provide the option to be exercised under form 10IE and form 10IF for section 115BAC and 115BAD.

CBDT amends Transfer Pricing Report to incorporate details with respect to transaction with companies opting concessional rate of tax under section 115BAB

Notification No. 82/2020 dated 01 October 2020

• Section 115BAB provides that if the Assessing Officer (AO) is satisfied that due to close connection between the company and any other person, the course of business is so arranged that the company produces more than the ordinary profits then he shall compute reasonable profits and gains of such company.

• For this purpose, AO may invoke the provisions of Section 92BA pertaining to the specified domestic transaction.

• The Form 3CEB has been amended to provide details in respect of these transactions.

Special Cash package equivalent in lieu of LTC Fare for CG employees MOF Press Release

Dated 12 October 2020

• In view of Covid-19 pandemic and resultant nationwide lockdown as well as disruption of transport and hospitality sector, Finance Minister Nirmala Sitaram has come out with a cash package for the CG employees.

• With a view to compensate and incentivize consumption by CG employees thereby giving a boost to consumption expenditure, it has been announced that- Cash equivalent of LTC comprising Leave Encashment and LTC fare will be paid by way of reimbursement if an employee opts for this in lieu of one LTC in the Block of 2018-21 subject to the certain conditions

• Amount to be spent by an employee = 100% of Leave encashment + 3 times the fare entitled

• The amount to be spent on purchase of items/services which carry a GST rate of 12% or above from GST registered vendors through digital mode.

• Amount to be spent on or before March 31, 2021

• TDS shall not be deducted on the reimbursement of deemed LTC fare.

CBDT notifies tolerance limit under transfer pricing for AY 2020-21 Notification No.83/2020 Dated 19 October 2020

The Central Board of Direct Taxes (CBDT) has notified that the tolerance limit of 1 per cent for wholesale trading and 3 per cent in all other cases for ALP determination during the Assessment Year 2020-21.

“Wholesale trading” means an international transaction or specified domestic transaction of trading in goods, which fulfils the following conditions:

a) The purchase cost of finished goods is 80 per cent or more of the total cost pertaining to such trading activities; and

b) Average monthly closing inventory of such goods is 10 per cent or less of sales pertaining to such trading activities.

Income Tax Department conducts Multiple searches. Press Release Bureau Dated 27 October 2020

• The Tax department has carried out multiple raids in the last week with seizure of documents and valuables worth hundreds of crores.

• The first search carried out on 22/10/2020 on a group of Assessee based in Srinagar.

• The search has led to a seizure of unaccounted cash amounting Rs. 1.82 Crores and Jewellery /bullion worth Rs.74 Lakhs, total undisclosed investments and cash transactions of Rs. 105 crore of the group, have been unearthed during the search.

• The Second search of 26.10.2020 was on a large network of individuals running the racket of entry operation and generation of huge cash through fake billing. The search operations have been conducted on 42 premises across Delhi- NCR, Haryana, Punjab, Uttarakhand and Goa

• The search has led to Documents accommodating around 500 crores entries also cash of Rs. 2.37 Crores and Jewellery worth 2.89 crores has been found along with 17 bank lockers, which are yet to be opened.

• The several shell firm/entities used by several operators for layering of black money and cash withdrawals against fake invoices have been investigated. The personal staff were made dummy directors. Statements of such entry operators, their dummy partners/employees, the cash handlers as well as the covered beneficiaries have also been recorded clearly validating the entire money trail.

Govt. notifies declaration cut-off date under Vivad se Vishwas Act, also extends payment timeline till March 31st Notification No. 85/2020, F. No. IT(A)/1/2020-TPL Dated 27 October 2020 & Circular No. 18 dated 28 October 2020

• Govt. notifies December 31st as the cut-off date for filing declaration under the Vivad se Vishwas Act, 2020

• Also, extends timeline from December 31st, 2020 to March 31st, 2021 for making payment without additional amount.

• Further, as per the existing provision of VsV Scheme the payment of taxes should be within 15 days of the receipt certificate from the designated authority. In order to relax the genuine hardship on the tax payer CBDT has clarified that 15 days criteria won’t be applicable if the declarant has applied for Vsv Scheme on or before 31st December 2020 and paid the taxes on or before 31st March 2021.

IT Department releases updated Schema for e-filing of Tax Audit Report Dated October 23, 2020

• IT Dept releases updated schema for e-filing of Tax Audit Report in Form 3CD

• Provides new drop down for selection of new concessional regimes u/s 115BA/115BAA/115BAB, also updates schedule for depreciation to incorporate adjustment made to the written down value under section 115BAA (for AY 2020-21 only)

• Incorporates new field to disclose all losses/allowances not allowed u/s.115BAA and adjustment for withdrawal of additional depreciation for opting for tax u/s.115BAA in the schedule for brought forward of losses

• Further, adds new drop-down list for mode of payment/repayment for Sec.269SS/Sec.269T purposes to include payment modes such as Debit/ Credit card, net banking, RTGS, NEFT, BHIM, etc

• Also releases schema change document listing out the changes in Form 3CD schema from initial schema release in August 2014 till 22nd October 2020.

Extension of Due Date of furnishing of Income Tax Return and Audit Reports Notification No.88/2020 29th October 2020

• In view of the challenges faced by taxpayer in meeting the statutory and regulatory compliances due to the outbreak of COVID-19, the government of India, Department of Revenue, Ministry of Finance and Central Board of Direct Taxes extended the due dates of filing of Income tax return and due date of furnishing of Audit report as follows.

CBDT notifies the Equalisation levy (Amendment) Rules, 2020 Notification No.87/2020 Dated October 28, 2020

• The Central Board of Direct Taxes (CBDT) had issued Equalisation levy Rules, 2016 (Rules) to lay down the procedural framework for compliances, forms for filing annual return and appeal process to be followed for equalisation levy.

• The Finance Act 2020 expanded the scope of equalisation levy, to include levy on consideration received or receivable by an ‘e-commerce operator’ from ‘e-commerce supply or services’.

• Now, CBDT has amended the Equalisation Levy Rules, 2016 as Equalisation levy (Amendment) Rules, 2020 to incorporate the amended provisions of equalisation levy on non-resident e-commerce operators. CBDT has also amended forms for filing annual statements and appeal before CIT (Appeals) and ITAT.

Taxpayers may have to pay interests on outstanding income tax exceeding Rs 1 lakh Hindustan Times, October 26, 2020

• The government on 28.08.2020 extended deadlines for furnishing various ITRs and audit reports as a relief to taxpayers from Covid-19 pandemic, but there is no clarification on the aspect of interest waiver.

• Taxpayers having tax outstanding exceeding Rs 1 lakh should not wait for the last date to file income tax returns (ITR) as they could be charged interest on the unpaid tax amount even as the government on 28.08.2020 extended the deadline for filing ITRs, officials and experts said.

• The CBDT (Central Board of Direct Taxes) has extended the due date for filing of the ITR for the Assessment Year 2020-21 to 31-12-2020 for non-audit cases and 31-01-2021 for audit cases, but no relief has been provided from the interest chargeable under Section 234A if the tax liability exceeds Rs. 1 lakh,”.

• “If self-assessment tax liability of a taxpayer exceeds Rs 1 lakh, he would be liable to pay interest under section 234A from the expiry of original due dates, i.e., 31-07-2020 or 31-10-2020. The interest under section 234A shall not be levied if the self-assessment tax liability of taxpayer does not exceed Rs 1 lakh and ITR is filed within the extended due date, i.e., 31-12-2020 or 31-01-2021

Some Case Laws

ITAT: Additional-evidence can’t be rejected absent prejudice to Revenue; Directs de-novo assessment Global One India Private Limited vs DCIT 12(1), New Delhi – ITAT Delhi ITA No.5165/Del/2016

• Delhi ITAT rejects CIT(A)’s decision to refuse admission of additional evidence by assessee in the form of audited financial statements filed for the first time during the appellate proceedings for AY 2004-05.

The assessee’s case was taken up for scrutiny assessment and during the course of assessment proceedings, the Assessing Officer (AO) asked the Company to provide audited accounts and details of expenses incurred by the Company during the year.

• However, due to lack of available data, the Company was unable to provide the said details.

• AO assessed the income at an ad-hoc 12%mark-up on total cost of providing services by the Company to its parent company.

• CIT(A) helds that the evidences were new, hence can’t be accepted.

• ITAT notes that “…correct income of the assessee can be determined only on the basis of the audited financial results” and thus, opines that “it would be incorrect to shut out an assessee in the process of administration of justice from leading evidence to prove its case”;

• The above evidences could not be filed earlier due to change in management from time to time which was beyond assessee’s control and also that the Company Law Board had compounded assessee’s offence,

• ITAT directs AO to make the assessment after duly considering the same and after giving proper opportunity to the assessee.

ITAT: Holds outstanding receivables as separate international transaction; Distinguishes Kusum Healthcare, Bechtel rulings Bharti Airtel Services Limited vs DCIT 4(2), New Delhi – ITAT Delhi ITA No. 161/Del/2017

• Delhi ITAT dismisses assessee’s appeal, holds outstanding receivables as a separate international transaction for Bharati Airtel Services for AY 2011-12

• In case of Kusum healthcare private limited, assessee has undertaken working capital adjustment for the comparable companies selected in its transfer pricing report which has not been disputed by the learned transfer pricing officer and therefore the differential impact of working capital of the assessee vis-à-vis is comparable had already been factored in pricing profitability and therefore the honourable High Court held that adjustment proposed by the learned TPO deleted by the ITAT is proper.

• In the present case there is no working capital adjustment made by the assessee as well as granted by the learned TPO.

Beneficial treaty rate preference u/s. 90 applies separately to each royalty agreement

IBM World Trade Corporation vs DIT I(1), – Karnataka High Court ITA No.278 of 2012

• Karnataka HC holds that the preference u/s. 90(2) for beneficial treaty rate shall applies separately to each royalty agreement entered pre & post June 2005; The assessee bifurcated the income based on the date of agreement and applied beneficial DTAA rate [15%] for royalty agreements dated prior to 1st June 2005 and tax-rate u/s.115A w.r.t for royalty agreements entered pre 1st June 2005.

• However, AO had taxed the entire royalty income at 15% on ‘aggregate’ basis without allowing assessee’s bifurcation based on agreement dates. Held that the income received by virtue of 2 different royalty agreements cannot be bifurcated for the purpose of computation of Income.

• HC also refers to CBDT Circular No.3/2014 explaining the amendment to Sec.115A(1)(b) vide Finance Act 2013, which corrected the “anomaly prevalent in Section 115A with regard to rates of taxes in case of non-resident taxpayer”.

HC Allows depreciation on 'revalued' intangibles to successor-company, rejects invocation of Sec.32(1) proviso Padmini Products (P) Ltd vs DCIT- Circle 12(2), Karnataka High Court ITA No.154 of 2014

• The assessee is a Private Limited Company engaged in the business of manufacturing, dealing in exporting of incense sticks and allied products. The assessee succeeded to, in the business of partnership firm viz., in terms of section Section 47(xiii).

• Before the firm was converted into private limited company, the partnership firm had revalued all its intangible assets at Rs.65 cr. which was transferred to assessee in consideration of share allotment at a premium.

• However while allowing depreciation to assessee, AO ignored the revalued figure and allowed it with respect to WDV.

• HC finds and rules that the aforesaid transaction is squarely covered u/s. 47(xiii) and therefore, was entitled for depreciation with reference to actual cost incurred by it with reference to intangible assets.

• On invocation of 6th proviso to section 32(1) (erstwhile 5th proviso) by Revenue, HC observes that until and unless it is the case of aggregate deduction, the proviso has no role to play. Moreover, HC holds that the 5th proviso in any case will apply only in the year of succession (i.e. 2005) and not in subsequent years.

• HC also overrules the applicability of Explanation 3 to Sec. 43(1) [which defines ‘actual cost’] as AO failed to establish that the main purpose of the transfer of such asset was reduction of liability to income tax by claiming extra depreciation on enhanced cost.

Expenditure incurred to acquire membership of stock exchange, a CAPEX eligible for depreciation BGSE Financials Ltd. vs DCIT- Circle 1(1)(2), Bangalore ITAT ITA No.3130/Bang/2018

• The assessee company is engaged in stock exchange operations. During the relevant assessment year, the assessee had made payment of Rs.11,34,836/- to MCX-SX Stock Exchange towards admission fees and processing charges. Assessee had claimed this as a revenue expenditure.

• The AO treated this fee as a capital expenditure and disallowed the same. The CIT(A) agreed with the view taken by the AO, however it allowed the depreciation on the admission fee paid.

• The Assessee argued that the fees paid as admission fees in a stock exchange is only a permission to do trading in shares and no capital asset is acquired by the assessee.

• In view of various SC cases, Bangalore ITAT concluded that the admission fee paid was a right or a license owned by the assessee and was used by him as an asset.

• Therefore, CIT(A) has rightly treated the admission fee as a membership of the stock exchange capital asset and allowed alternative plea of assessee that depreciation is to be granted on the same.

While kidnapping is an offense, paying ransom is not Khemchand Motilal Jain, Tobacco Products(P) Ltd.,Sagar vs CIT, Madya Pradesh HC ITR NO.42/1998

Just for Laughs..

• The assessee engaged in manufacture and sale of bidis, sent its whole-time director to a forest area for purchase of tendu leaves. There, the director was kidnapped by dacoits and the assessee paid ransom of Rs. 5.50 lakhs to secure his release after the police failed to rescue.

• The AO disallowed the claim for deduction of the said amount u/s 37(1) though the CIT (A) and Tribunal upheld the claim on the ground of commercial expediency. Before the High Court, the department relied on the Explanation to section 37(1) and argued that expenditure incurred for any purpose which is an offence or which is prohibited by law is not allowable as a deduction.

• While kidnapping for ransom is an offence u/s 364A of the IPC, the payment of ransom to secure the release of a kidnapped person is not an offense. The payment of ransom is not prohibited by law. Accordingly, the Explanation of to section 37 (1) is not applicable and the ransom is deductible as business expenditure.

Nike India's distribution of sample promotes parent's brand; Upholds disallowance u/s. 37 Nike India Pvt Ltd Vs ACIT IT(TP)A Nos.330/Bang/2015, 804/Bang/2016 356/Bang/2017, 739/Bang/2017 & 3321/Bang/2018

• Bangalore ITAT upholds disallowance u/s. 37 of cost of samples distributed by Nike India (assessee-company)

• Burden of incurring expenditure on samples was on the parent co. [i.e. Nike Inc.];

• Notes that Nike Inc. introduced new products and in order to create an awareness supplied the samples of such products to the assessee for distribution amongst the distributors;

• Holds that “The assessee herein is merely an intermediary between M/s Nike Inc and the public.”;

• Sample expenses are related to brand promotion and marketing initiatives of the parent company of the assessee and such expenditure is not meant for the assessee’s business;

• Further opines that in trade circles, it is known fact that the expenditure on samples are borne by the manufacturers only

No malice in tax deduction at lower rate on property purchase; Deletes penalty Shri Jitendra Sharma & Ors Vs JCIT ITA Nos. 500 to 502/Ind/2018

• Indore ITAT deletes penalty levy u/s. 271C in respect of TDS wrongly deducted u/s 194-IA @1% instead of Sec. 195 @ 20.6% on purchase of property from a Non Resident considering no documentary evidence provided by the seller except PAN

• ITAT remarks that merely having a local address in USA [in the sale deed] cannot be a sufficient evidence to show that the person is an NRI;

• Observes that subsequently when the assessee were brought to the notice that the seller is an NRI pursuant to TDS default proceedings u/s. 201, “they as law abiding citizens immediately deposited the correct amount of TDS @20.6% …. along with interest….”,

• “It would have made no difference for them to deduct tax @1% or 20.6% since it was to be withheld from the purchase consideration.”

No penalty for wilful attempt to evade tax if assessee couldn’t furnish ITR due to seizure of books of account Kewalchand M. Kothari v. DCIT - [2020] 120 taxmann.com 91 (Madras)

• A search was conducted and books of account of the assessee was seized.

• On the due date of filing of return in the year in which search was conducted, the books didn’t handover to the assessee and accordingly, assessee filed the belated return and paid entire demand made by DCIT and acknowledged the same.

• Assessee voluntarily disclosed the undisclosed income on the search conducted under section 132

• Therefore, there was no intention to wilful evade the payment of taxes. Admittedly, the DCIT had seized the relevant books of account and assessee could not able to file the return of income on or before the due date.

• Therefore, the offence under section 276C(2) was not attracted at all. The entire criminal proceedings pending against the assessee was nothing but clear abuse of process of law.

Discretionary hearing opportunity under ‘Faceless Appeal Scheme’ challenged before Delhi HC Lakshya Budhiraja v. Union of India & ANR. W.P. (C) 8044/2020 16-10-2020

• Writ petition seeking a direction to grant an opportunity of hearing to all taxpayers and should not be at the discretion of the Chief Commissioner (CC) or the Director-General (DG) as proposed in the Faceless Appeal Scheme, 2020.

• Faceless Appeal Scheme, 2020, is discriminatory, arbitrary and illegal to the extent it provides a virtual hearing as per the circumstances to be approved by the administrative authorities.

• Taxpayers may or may not provide a right of personal hearing in the matter.

• This mechanism violates Article 14 of the Constitution of India

• The right to provide or not to provide a hearing in the matter is also against the principle of audi alteram partem, i.e., no person should be judged without a fair hearing in which each party is given an opportunity to respond to the evidence against them. The Faceless appeal scheme is contrary to sub-sections (1), (2) and (5) of Section 250 which specifically state that the right of hearing shall be granted to an assessee at the appeal stage.

Excess credit period allowed to AE amounts to international transaction and FOREX gain is part of operating income LSI India Research & Development Pvt Ltd Vs DCIT IT(TP) A No.3170/Bang/2018

• Bangalore ITAT rules on TP-adjustment in respect of trade receivables, treatment of foreign exchange (FOREX) gains

• “non-charging or undercharging of interest on the excess period of credit allowed to the AE, for the realization of invoices amounts to an international transaction and the ALP is required to be determined”.

• Outstanding receivable partake the character of “capital financing” included in the definition of “international transaction” and consequently, overdue outstanding is an international transaction.

• ITAT directs PLI computation by treating FOREX gains having nexus with international transaction as part of operating income, follows coordinate bench decision in e4e Business Solutions.

Data of audited financials to be considered and not of prowess database. Basell polyolefins India Pvt Ltd vs ACIT ITA Nos. 4724 & 4725/MUM/2016 12th October 2020

• The Assessee is engaged in the business of rendering project, engineering and polyolefins product related services. During AY 2009-10 it had filed its return of income and the same was selected for scrutiny and then transferred to TPO for benchmarking the transaction with AE.

• The Assessee while preparing the TP documentation relied on the prowess data base for 4 companies as audited financials were not available at that juncture. During the course of hearing the Assessee submitted the audited financials of 4 comparables and asked to revise the OP/OC margin. The TPO rejected Assessee’s contention and also conducted fresh search process with 15 new comparable and made 1.2 cr adjustment accordingly the AO passed the order with adjustment.

• The CIT –A removed 2 companies from AO’s comparable of 15 companies and granted relief of only around 26 Lakhs.

• The Assessee filed appeal with ITAT for change in OP/OC of 4 comparables and inclusion of 4 New comparable as CIT-A have agreed that insurance broking companies is closely comparable with the Assessee Business.

• ITAT in the order has accepted assessee contention of Audited financials as against prowess data base and inclusion of 4 new companies based on the new search process.

Goods and Services Tax

GST litigation update Liaison office of a foreign company is liable to obtain GST registration

The Karnataka Authority for Advance Rulings (AAR) recently had an occasion to determine taxability of activities undertaken by the liaison office in India. The applicant in this case viz. M/s Fraunhofer-Gessellschaft Zur Forderung der angewwandten Forschung e.V, Germany – Liaison Office posed three questions before AAR: (i) whether activities undertaken by them in India amounts to “supply” under GST law? (ii) whether liaison office is required to be registered under the CGST Act and (iii) whether liaison office is liable to GST?

It is worthwhile to note that, in terms of extant FEMA Regulations, liaison office can only act as a channel of communication between its head office and entities in India and it cannot generate income in India and cannot engage in any commercial / trading / industrial activity.

The Karnataka AAR in this case noted that RBI’s injunction on business of the applicant cannot decide the scope of business for the purpose of GST. By referring to the various definitions and scope of the term “supply” under the CGST Act, AAR held that the activities of the applicant squarely fit under the scope of the term “supply” even in the absence of consideration. Thus, applicant would be required to obtain GST registration. AAR also held that activities of the applicant liaison office in this case would fall under the definition of “intermediary services” and applicant would be liable to pay GST if the ‘place of supply’ of services is in India.

Above Ruling has created fresh set of controversy as regards GST implications on liaison office of foreign companies in India. Earlier on similar issue, Rajasthan AAR and Tamil Nadu AAR had held that liaison office is not required to obtain GST registration as in terms of RBI permission issued to them they do not have any source of income in India and they cannot undertaken any commercial activity in India.

Notional interest on security deposit includible in value of supply

The Karnataka AAR in the case of M/s Midcon Polymers Pvt Ltd. held that notional interest on security deposit in relation to renting of immovable property service is includible in value of supply, that is, rental income, if it influences the value of rental income. In the present case, the appellant proposed to collect an amount of ₹5 crores as security deposit for a monthly rent of ₹1.5 lacs. AAR noted that security deposit is taken invariably in all cases and it is a general practice that wherever the quantum of deposit is higher the rent charged is less. AAR also noted that there is a nexus between security deposit taken and the rent charged and that the notional interest that the applicant would earn is in respect of renting service. Thus, the notional interest has to be considered as a part of value of supply of service if the said notional interest influences the value of rental income and would be taxable at the rate applicable to rental income.

Taxability of supply of soft beverages/aerated water and cigarettes by a 5-Star Hotel, canteen services provided free of cost to employees liable to GST

The Tamil Nadu AAR has held that supply of soft beverages/aerated water whether in person or as room service, by the restaurant located in the premises of the 5-Star hotel is taxable at the rate 18%. Interestingly in this case the applicant claimed that supply of soft beverages/aerated water alone in a restaurant is not a composite supply and they were discharging GST liability at the rate of 28% along with applicable compensation cess. The AAR noted that when a guest comes to the restaurant and orders only soft beverages/aerated water, it involves supply of goods (soft beverages/aerated waters) and supply of services by the restaurant in the form of use of the facilities of the restaurant. As these two are naturally bundled and supplied in conjunction each other, it is a ‘composite supply’ in which principal supply is that of a restaurant service and is taxable at 18%.

As regards sale of cigarettes with similar facts as above, the AAR however noted that sale of cigarettes is not naturally bundled together with the restaurant services as the services of the restaurant involve serving of food and beverages alone in the normal course. Thus, the AAR concluded that sale of cigarettes in the restaurant of the 5-Star hotel is a ‘mixed supply’ and would be taxable at the rate of 28% along with compensation cess.

On the question of free food provided to employees in a separate canteen as a part of the employment contract, the AAR has held that the same would be considered as supply of services without consideration in terms of Schedule I to the CGST Act and hence would be liable to GST at 18% on the value to be determined under GST Valuation Rules.

GST at 18% applicable in case of reimbursement of credit card expenses to foreign holding company

The Tamil Nadu AAR has held that reimbursement of credit card expenses to foreign holding company is liable to GST as import of services at the rate of 18%.

The facts in this case are that the applicant viz. M/s ICU Medical India LLP is engaged in the business of software development for its ultimate holding company in USA. Holding company in USA by virtue of its arrangement with Wells Fargo Bank, USA provides credit card to the employees of all the group companies located globally. Employees of the applicant use this card for incurring travel expenses both in India and abroad towards tickets, food and accommodation etc. It was stated by the applicant that the Credit cards are property of holding company and settlement of credit card bills with Wells Fargo Bank is done by the holding company who in turn claims reimbursement at actuals from the applicant by raising an invoice.

The Tamil Nadu AAR noted that there exists a separate transaction between the applicant and its holding company for the services of providing the credit cards to the employees of the applicant and for this, a payment is made by the applicant to holding company. Further the services are provided by the holding company on its own account and not as ‘intermediary’. Thus, AAR concluded that holding company is supplying credit services to the applicant which fall under the definition of ‘supply’ under GST law and are liable to tax at the rate of 18% as import of services in India.

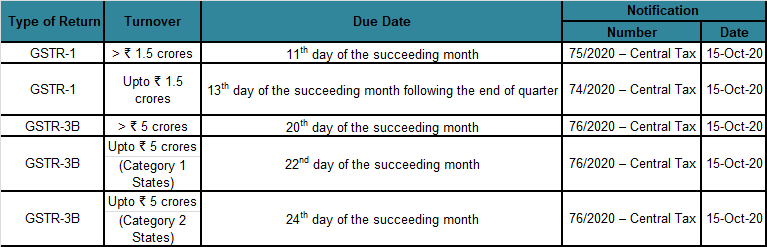

Due Dates

GST Compliance calendar

Category 1 States: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

Category 2 States: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi

GST Annual Return and Audit Report update:

• Government makes filing of GST Annual Return in Form GSTR-9 optional for taxpayers having aggregate turnover up to ₹ 2 crores for the financial year 2019-20

• Turnover threshold for GST Audit for the financial year 2019-20 increased to ₹ 5 crores

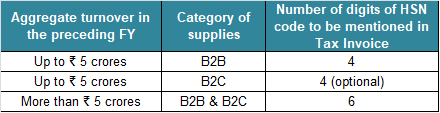

Government mandates six-digit HSN code in Tax Invoice from April 1, 2021

With effect from April 1, 2021, HSN code reporting in Tax Invoice would be as follows:

Singapore Due Dates

GST: August to October – November 30 Form CS: 30th November ACRA Annual Return Year ending 30th April: 30th November

Other updates/News Oman introduces CbCR; Clarifies purpose to assess high-level TP, BEPS risks

• Oman introduces Country-by-Country Reporting (CbCR) requirements vide Ministerial Decision 79/2020;

• CBCR applies to MNE headquartered or operating in Oman, effective for fiscal years commencing on or after January 1, 2020, and will apply to MNE groups having consolidated revenue of at least Rial Omani 300 million in the fiscal year immediately preceding the reporting period reflected in the consolidated financial statements for such preceding year;

Thailand reduces penalty for delayed TP-disclosure forms e-filed by 30 Dec 2020 amidst Covid-19 Pandemic Thailand Revenue Department News

• Thailand Revenue department, owing to the outburst of Covid-19 Pandemic, announces a relief by way of reducing the penalty (from 200,000 baht to 5000 baht) for delayed submission of transfer pricing “disclosure form” to economically distressed taxpayers affected adversely by the pandemic

• The original due date for submitting a Disclosure Form for a related company or juristic partnership firm earning total income of not less than 200 million baht for the accounting period starting on or after 1st January 2019 was 31st August 2020;

• By virtue of this announcement, the taxpayers can now e-file the Disclosure form with revised penalty rate within 30th December 2020

• In addition to this, the department also increases the channels to submit disclosure forms in the form of excel files in order to facilitate fast and convenient e-filing for the taxpayers.